The impact of the coronavirus crisis on Belgian companies’ turnover is fading only slowly and the outlook for 2021 is still gloomy

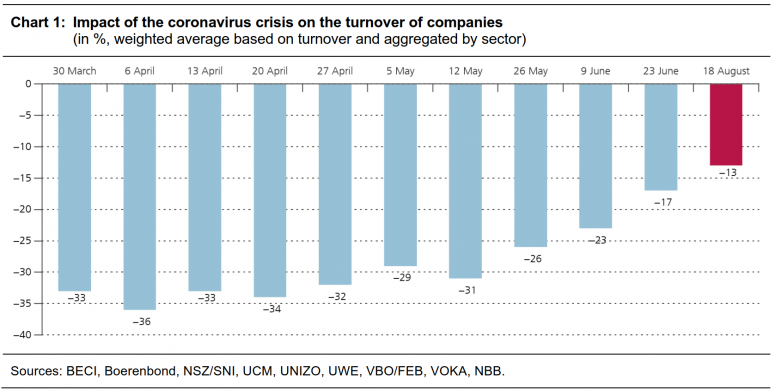

Brussels, August 2020 – Belgian firms estimate that their turnover is currently still 13 % below normal levels. This is certainly an improvement on the situation at the end of June (+4 percentage points) but the recovery is looking sluggish. Moreover, companies are expecting their turnover next year to still be 10 % below the norm. These are the salient points of the latest ERMG survey among Belgian firms. The survey also reveals that, for two out of every three companies questioned, the crisis will have a lasting effect on the way of working like encouraging more intensive teleworking or fewer business trips.

A new survey was conducted last week by a number of federations of enterprises and the self-employed (BECI, NSZ/SNI, UCM, UNIZO, UWE and VOKA). The initiative is coordinated by the NBB and the FEB/VBO. This latest survey follows on from a series of ten waves of surveys conducted between March and June, with the aim of assessing the impact of the coronavirus crisis on economic activity in Belgium and on the financial health and decision-making of Belgian companies. This series of polls had been temporarily suspended during the two main summer holiday months, not least because there would have been a very low number of respondents. In all, 4 430 companies and self-employed people responded to this survey[1]. The changes in the indicators cited should be interpreted with caution, in view of the long time gap between this survey and the previous one. A survivor bias may therefore appear, especially within certain sectors. It is possible that some companies in difficulty have meanwhile filed for bankruptcy and are therefore no longer taken into account in this survey. Moreover, the respondents are different from those from the previous survey (owing to UCM’s participation, for instance). It nevertheless seems that the composition of this week’s sample of firms better reflects the sectoral and regional composition of the Belgian economy than in the previous surveys.

[1] Participation in the survey by some federations whose members operate in a specific sector of activity may lead to a sampling error. In particular, companies from one by branch of activity could be more strongly represented in our sample than in the Belgian economy as a whole. The sample is therefore stratified by industry based on the weight in value added in Belgium. Note that the changes over the weeks should be interpreted with caution, as the companies that reply to the survey are not necessarily the same each week. It should also be noted that the figures may differ slightly from previous publication figures due to the inclusion of data received afterwards and because the data analysis is constantly being refined.

Company turnover continues to improve, albeit slowly

Taking account of company size and sectoral value added, firms questioned this week reported a 13 % drop in their turnover from the norm. By way of illustration, that figure was still as high as 17 % at the end of June. So, the improvement is continuing but it remains sluggish. The lack of demand is by far the main reason for the loss of turnover in almost all sectors. At regional level, this week’s survey shows that the impact perceived by firms questioned is greater in Wallonia and Brussels than in Flanders.

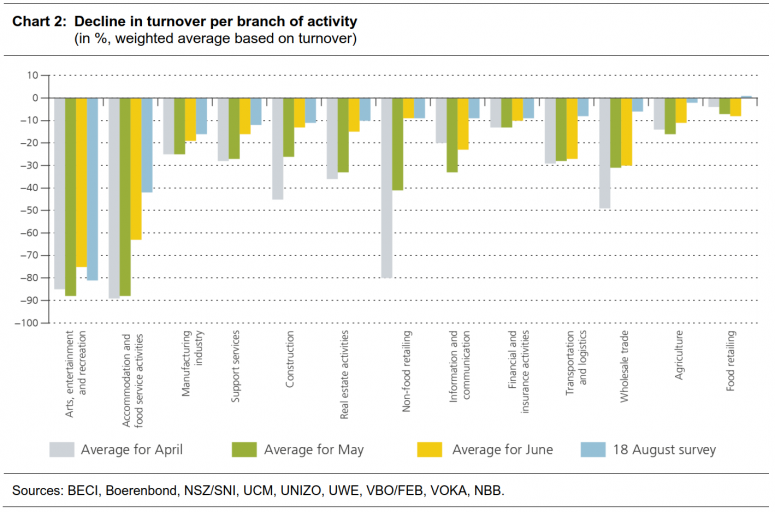

As in previous surveys, there is a noticeable difference between the various branches of activity. The arts, entertainment and recreation sector is still by far the worst-hit branch of activity since, even as recently as this week, firms from this sector were reporting an 81 % collapse in their turnover from normal levels. This figure is in line with those recorded in the surveys during the second quarter. The reasons for this fall cited the most often are the prohibition of certain activities and weak demand (for respectively 71 and 50 % firms surveyed).

The second most badly affected sector is still catering and accommodation with revenue losses of 42 % from normal levels, compared with a drop of as much as 50 % at the end of June. The reopening of bars and restaurants in June had exerted a positive and significant impact on their revenue, but the improvement has been weak since then. The reasons most often cited by catering and accommodation businesses to explain this reduction are weak demand and applying the hygiene and social distancing rules in practice (for 46 % of respondents in both cases).

Manufacturing industry enterprises surveyed point to a decline of 16 % from the norm. The low level of demand appears to be by far the most important reason and is cited by more than six firms out of every ten questioned. That may be a sign that the recovery in international trade and thus in foreign demand remains slack for the time being.

As for the outlook for next year, only a very slight improvement in revenue is anticipated by the companies surveyed. They are effectively expecting a 10 % drop on normal levels in 2021. A sluggish recovery of business activity seems to be the scenario foreseen by the vast majority of branches of activity. For the arts, entertainment and recreation sector and catering and accommodation – the two worst-hit sectors at the moment – the anticipated revenue losses for 2021 still come to respectively 44 and 37 % of normal levels. The construction sector as well as support services also exceed the national average with anticipated losses in their revenue of respectively 13 and 11 %.

The risk of bankruptcy and degree of concern have increased since June

The perception of risk of bankruptcy seems to have got worse in this survey. More specifically, 8 % of the companies surveyed reckon that bankruptcy is either likely or highly likely. In the survey carried out on 23 June, this proportion reached 5 %. It is among firms questioned from the arts, entertainment and recreation sector, the transport and storage sector and catering and accommodation that the risk of bankruptcy is observed as being high (respectively 30, 24 and 20 %). Moreover, a regional difference also seems to be emerging and the perception of the risk of bankruptcy is considerably higher in Wallonia and Brussels than in Flanders.

The slight rise in the risk of bankruptcy may be related to the composition of our sample in connection with the participation of the different business federations. On the other hand, it is possible that some companies in difficulty have meanwhile filed for bankruptcy and are therefore no longer taken into account in this survey (what is referred to as the “survival bias”). By way of example, companies questioned reckon that no less than 9 % of firms in their own sector of activity have filed for bankruptcy or started insolvency proceedings as a result of the coronavirus crisis. This figure is even over 30 % for catering and accommodation and for the arts, entertainment and recreation sector. The fact that companies going into bankruptcy are no longer taking part in the survey suggests that the negative impact of the coronavirus crisis could well be under-estimated.

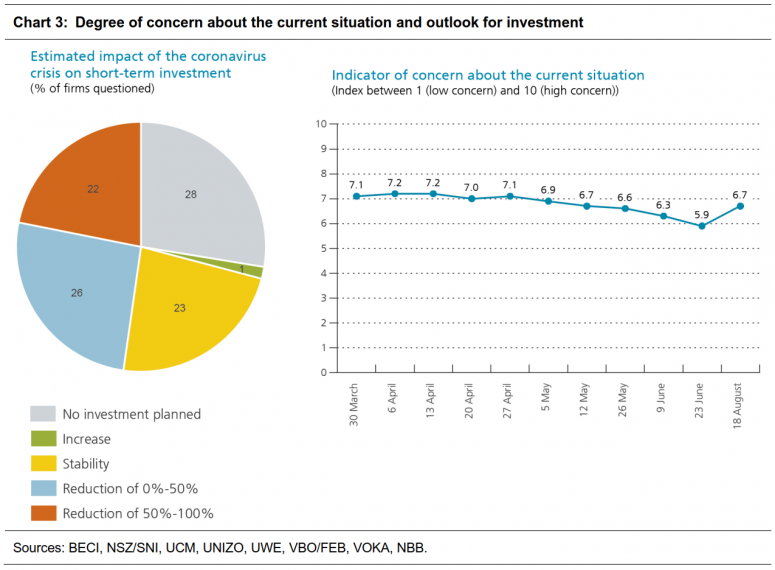

The degree of concern about the company’s business activity, measured on a scale of 1 (low concern) to 10 (high concern), has deteriorated this week from the end-of-June findings. Firms questioned indicated a level of 6.7 this week compared with 5.9 at the end of June. The current level is comparable to numbers recorded in mid-May. It is highly likely that the resurgence in the number of positive cases of COVID-19 in the last few weeks and the tightening up of measures have triggered a rise in concern. As the degree of concern remains high, it is logical that no real recovery has been observed in investment planned in the short term. On this subject, firms questioned say their investment plans have been scaled back by one-third from pre-coronavirus crisis forecasts, a similar figure to that observed in June.

Turning to liquidity problems, firms surveyed have not reported any improvement on the situation back in June. Over the last week, three out of every ten firms surveyed said they had hit liquidity problems, a similar result to that observed in June. The two main reasons behind these liquidity problems are a fall in revenue (for 19 % of respondents) and late invoice payment by clients (for 17 % of respondents). Limited access to credit is the third most often cited reason and only concerns 8 % of firms surveyed.

The impact on private employment remains high and new ways of working are becoming permanent

The coronavirus crisis continues to have a strong impact on the labour market, both in terms of number of jobs, unemployment (temporary lay-offs) and ways of working. On the employment front, firms taking part in the survey are expecting a 2 % drop in the period between the beginning of the crisis and the end of the year, the loss of just over 50 000 workers. In the second quarter, a higher number had been put forward but it is worth bearing in mind that the survival bias makes any comparison between the two dates difficult (companies that have filed for bankruptcy since June have already triggered a drop in employment) and also, in the space of two months, the context has changed (notably as regards temporary lay-off measures that have been extended, which could put off redundancies to next year). The number of student jobs has also dropped this summer: firms surveyed point up a 30 % fall in student employment from the normal situation; only the agriculture and food retailing sectors report a ‘‘normal’’ level.

Although it has been scaled back considerably, the temporary lay-off scheme is still being used by many firms. According to the survey findings, over the last week, 6 % of private sector workers were still on temporary lay-off, compared with 11 % at the end of June. Temporary lay-offs remain largely concentrated in catering and accommodation (21 % of employment) and in the arts, entertainment and recreation sector (57 % of employment).

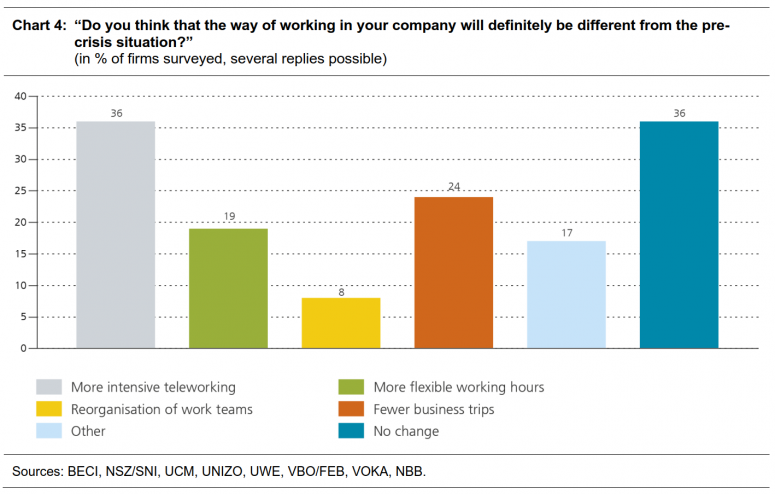

Finally, as a result of the coronavirus crisis, the way of working has been adapted in many companies, and for two out of every three firms surveyed, this adjustment likely to become permanent. In particular, even in the future, employees are expected to be given greater flexibility in their working arrangements, either via wider recourse to working from home (for 36 % of firms surveyed), or through more flexible working hours (for 19 % of firms surveyed). According to the survey, one in every four companies expects to cut back on the number of business trips. Obviously, these changes to the way of working depend on the company’s branch of activity. More intensive use of teleworking, for example, concerns principally the information and communication, financial and support services sectors. On the other hand, the reduction in the number of business trips is mentioned more in industry.