Business turnover continues to recover slowly but the outlook is becoming a little gloomier

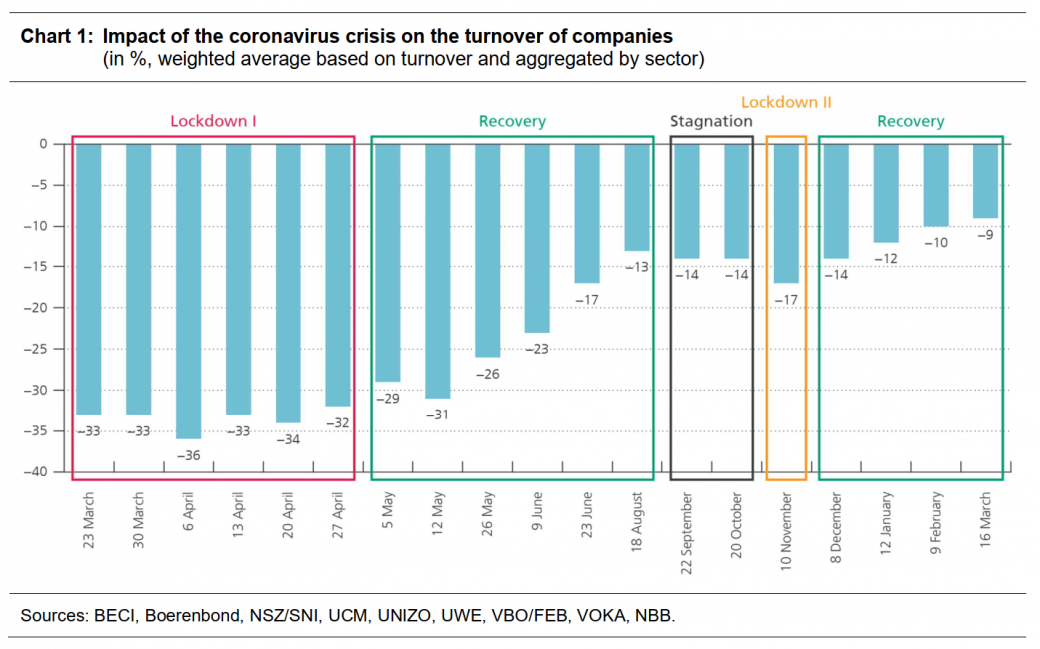

The loss of turnover suffered by Belgian firms owing to the coronavirus crisis is down again slightly from 10 % in February to 9 % in March. The strongest improvement comes from the non-medical contact professions, although their loss of turnover is still considerable. In contrast, the outlook for firms in 2021 and 2022 has deteriorated slightly, possibly because the health crisis is persisting for longer than expected. Those are the findings of the latest ERMG survey of Belgian firms, conducted at the beginning of last week, i.e. before the Consultative Committee postponed the planned easing of restrictions last Friday. In general, it is therefore probable that the results do not yet reflect the increased likelihood of further restrictions. The survey also reveals that firms expect to reduce their office space per employee considerably – by an average of 9 % - over the next five years. That is clearly due to a structural rise in home working, and that percentage is also significantly higher for large firms and for those based in Brussels, and for businesses that rent their office space.

Last week, a number of federations representing businesses and the self-employed (BECI, Boerenbond, NSZ/SNI, UCM, UNIZO, UWE and VOKA) conducted a new ERMG survey. This initiative is coordinated by the NBB and the FEB/VBO. It was the nineteenth in a wave of surveys carried out since March 2020, aiming to assess the impact of the coronavirus crisis and the restrictive measures on economic activity and the financial health of firms. In total, 3 884 firms and self-employed persons took part in the survey this week[1]. With the participation of Boerenbond, there were numerous respondents from the agricultural sector this time, so that the results give a more accurate picture of that branch of activity than in previous months.

The survey took place mainly on 15 and 16 March. The results therefore do not yet fully reflect the latest deterioration in the health situation in Belgium (as elsewhere in Europe) nor, in particular, the fact that the planned easing of restrictions was postponed by the Consultative Committee, brought forward to 19 March. That move undoubtedly had an adverse impact on the expectations of firms directly or indirectly affected, such as those in the arts, entertainment and recreation sector.

Belgian firms report a new, slight improvement in their turnover in March

Taking account of firms’ size and the sectoral value added, the firms polled last week stated that their turnover was down by 9.3 % compared to normal. That represents a very small improvement of one percentage point against the February survey, but a more substantial 8 percentage point improvement on the November figure. The fall in turnover is again smaller in the Flemish Region than in the Brussels-Capital Region and the Walloon Region.

[1] The ERMG survey is based on the opinions of the firms taking part. Comparison of the results over time should therefore be interpreted with a degree of caution, because the firms questioned may vary from one survey to the next. First, it is always possible that the federations conducting the surveys of their members may not be the same. Also, firms do not participate systematically in every survey. Although we correct any over-representation in the sample of firms from certain sectors, it is possible that the firms polled may vary according to other characteristics as time goes by.

The biggest improvement was naturally recorded by the non-medical contact professions, most of which were able to resume their activities. Their loss of turnover was halved compared to the previous survey conducted at the beginning of February, although it still amounts to 40 %. The other sectors of activity have seen far less change in their loss of turnover. A small improvement was recorded in some major sectors of the Belgian economy, notably support services, construction, information and communication, wholesale trade and food retailing. Conversely, the loss of turnover increased in real estate activities, agriculture and non-food retailing. The reduction in the loss of turnover recorded in this last sector in January and February was therefore only temporary and was probably due to the extended seasonal sales period. Finally, the loss of turnover is still very substantial for travel agencies (91 %), road passenger transport (81 %), accommodation and food service activities (78 %) and the arts, entertainment and recreation sector (73 %).

Although weak demand is still the most commonly cited reason for the loss of turnover (43 % of respondents), the frequency with which it is mentioned has declined steadily since August, which may be a sign that the recovery is gaining strength. In addition, the restrictions continue to depress turnover, particularly in certain sectors of activity. The ban on certain activities remains the principal obstacle for travel agencies and firms in accommodation and food service activities and the arts, entertainment and recreation sector. Implementation of the rules on hygiene and social distancing likewise lead to a loss of turnover for many respondents in the non-medical contact professions. Finally, since January there has been a marked increase in supply chains problems in some sub-sectors of manufacturing industry (particularly the manufacture of electrical machinery and appliances, electronic, optical and IT products, furniture and transport equipment), in logistics and in the wholesale trade.

As in previous surveys, self-employed persons and small firms report a much greater impact of the coronavirus crisis on their turnover than large firms. On average, self-employed persons report a decline of almost 36 % compared to normal, while large firms record an average decline of 6 %. Nevertheless, the gap narrowed slightly in March, since the turnover of non-medical contact professions recovered significantly, and that sector comprises mainly self-employed persons and very small firms.

Firms became slightly more pessimistic for 2021 and 2022

For the year 2021, the firms polled expect sales to be 8 % lower than they would have been without the coronavirus crisis, while in 2022 the loss is still put at 4 %. That represents a small, one percentage point deterioration compared to the survey conducted at the beginning of February. For the sectors still seriously affected by the restrictions, the deterioration is considerably greater, the likely reason being that the health crisis is persisting for longer than had originally been expected. The predicted loss of turnover in 2022 is now higher than 20 % in accommodation and food service activities and in the arts, entertainment and recreation sector, and actually higher than 30 % for travel agencies, road passenger transport and aviation.

The investment outlook improved slightly in March but nevertheless remains relatively gloomy: the average firm expects its investment to be 18 % below normal in 2021 owing to the coronavirus crisis, and will still be 11 % down in 2022.

On the subject of the employment outlook in the private sector, the firms polled now expect a net rise of 14 000 units, compared to 18 000 in the February survey. Employment is expected to be down by around 10 % in the hardest hit sectors, but that will be more than offset by a small rise in certain sectors representing a larger share of employment, notably support services, industry, construction, and information and communication. That said, the ultimate impact on employment will also depend on the success of the labour market policies aimed at facilitating transitions between sectors of activity. It should also be noted that these figures only concern employees and that the total impact on private sector employment should also include self-employed workers who go out of business as a result of the coronavirus crisis.

Perceptions of the bankruptcy risk and liquidity problems are also improving slightly

While hardly any of the firms questioned stated that they were currently undergoing a bankruptcy procedure, 4.5 % of respondents said that they expected to apply for bankruptcy in the next six months, a one percentage point improvement compared to the February survey. The main reduction in the bankruptcy risk is in accommodation and food service activities, travel agencies, non-medical contact professions and the arts, entertainment and recreation sector, probably owing to the timetable for easing restrictions announced at the beginning of March. However, that assessment is likely to be too optimistic now that the easing of restrictions has become more doubtful and the health situation has deteriorated again.

The proportion of firms facing liquidity problems has remained relatively stable, at 32 % of those polled. The main reasons for these liquidity problems are loss of turnover (16 %) and late payment by customers (11 %). The proportion of firms needing an additional capital injection or supplementary loans within a maximum of three months in order to meet their current financial liabilities has declined from 19 % in February to 16 % in March.

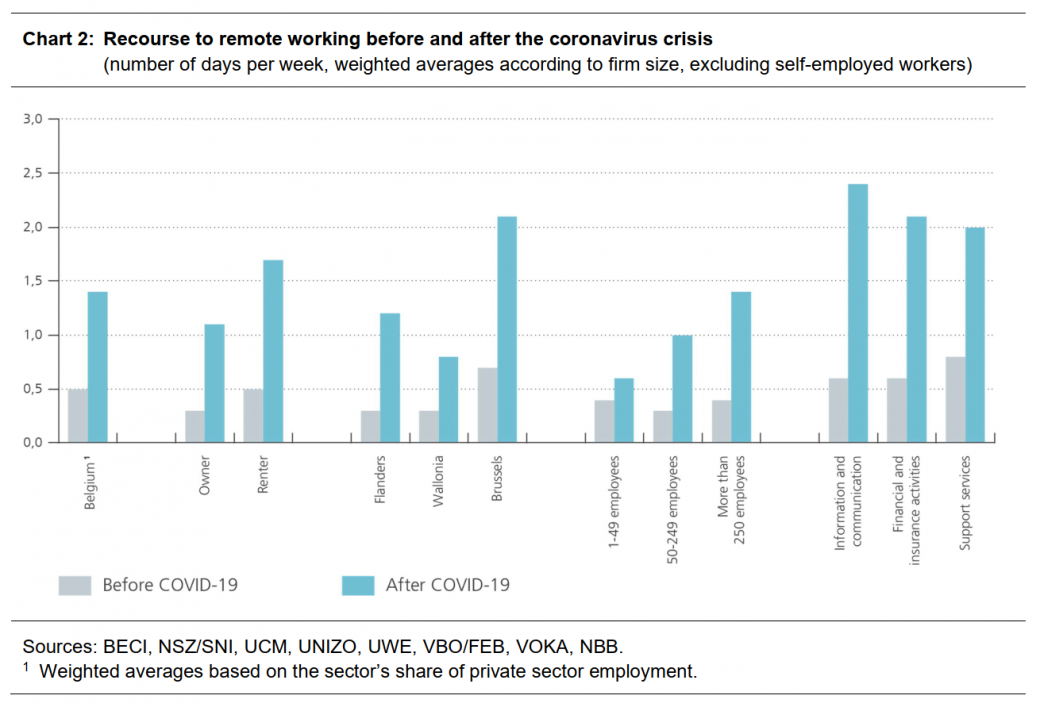

Home working will become almost three times more common after the crisis than before

In March, the firms polled stated that 32 % of their staff were working entirely from home and 15 % partly from home. According to the survey’s findings, recourse to home working has been fairly constant since it became mandatory in November for all jobs for which it is technically feasible. By way of illustration, home working is now slightly higher than in the April surveys. However, it should be pointed out that, at that time, almost a third of workers had been temporarily laid off, compared to 7 % today.

The firms questioned expect recourse to home working to increase after the coronavirus crisis, too: the average number of days per week spent working at home will almost triple, from 0.5 days before the crisis to 1.4 days after the crisis. That last figure is only slightly lower than the current figure of 2.1 days per week working at home. The expected recourse to home working after the crisis is considerably greater for firms in the Brussels-Capital Region (2.1 days per week) and for certain sectors of activity, notably information and communication (2.4 days per week), banking and insurance (2.1 days per week) and support services (2.0 days per week). It is also greater for large firms and companies that rent their office space instead of owning it.

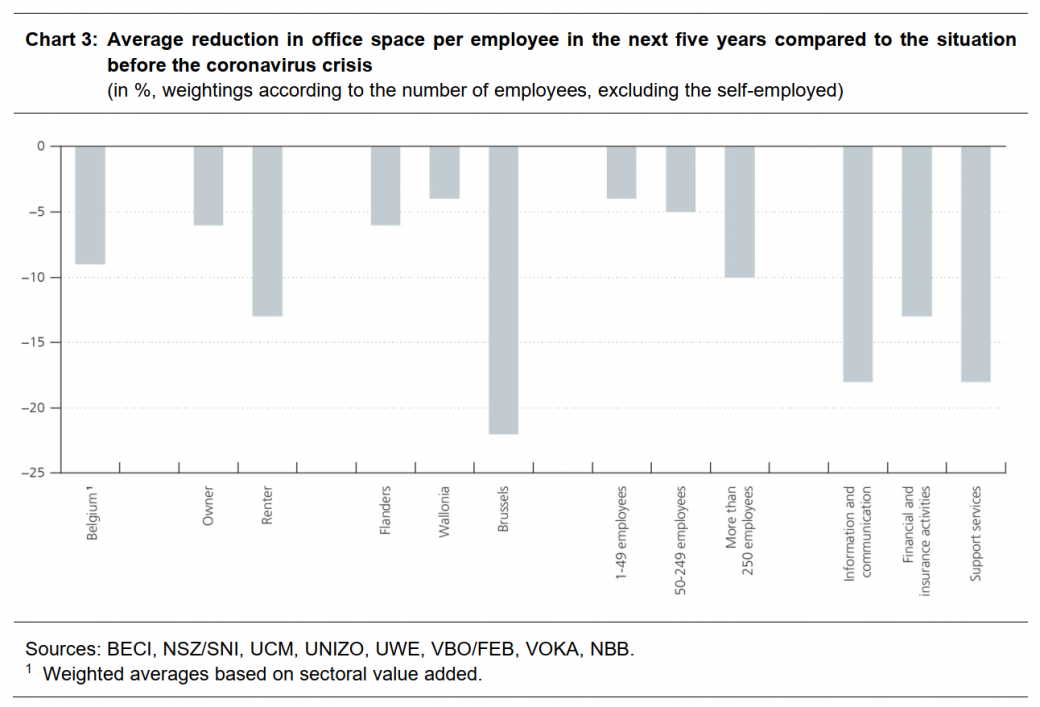

Firms will use significantly less office space in the future, especially in the Brussels-Capital Region

The increased importance of working from home has implications for the office space needed. In the March survey, the firms polled were asked how their office space per employee would change over the next five years, compared to the situation before the coronavirus crisis. On average, a 9 % reduction is currently expected. Of course, the decline is steeper in the sectors which will make more use of remote working after the crisis[2], particularly banking and insurance (‑13 %), support services (-18 %) and information and communication (-18 %). The expected reduction is also greater in the Brussels-Capital Region (-22 %, compared to -6 % in Flanders and -4 % in Wallonia), which may not be due solely to the trend towards increased working from home.

[2] The results show that the level of home working after the crisis is a more important determinant of the decrease in office space than the increase in home working compared to the pre-crisis level.