Operation of the guarantee scheme (envelope, calculation of losses, etc.)

4.6 What is the budget for the second guarantee scheme?

One fifth of the € 50 billion budget for the first guarantee scheme will be transferred to the second guarantee scheme. This means that, under the second guarantee scheme, loans with a maximum joint principal of € 10 billion are eligible for the State guarantee.

4.7 How exactly does the second guarantee scheme work?

All banks can include part of the envelope in new additional loans and credit lines in proportion to their market share in outstanding loans and credit lines (all loan terms) granted to viable non-financial businesses, SMEs, self-employed persons and non-profit organisations on 31 December 2019. This market share was ascertained on the basis of FINREP (table 20.04) and scheme A (table 02.11) reporting and notified to all institutions by individual standard NBB letter of 14 April 2020. Institutions may use up to 20% of the envelope thus allocated to them to grant guaranteed loans under the second guarantee scheme.

Unlike the first guarantee scheme, the second guarantee scheme is optional. Consequently, at the moment a loan is granted, the lender should specifically identify the loans he wishes to include in the guarantee scheme. In other words, the choice for the guarantee scheme is made (at the latest) at the moment the loan is granted, subject to the agreement of the borrower.

The guarantee applies to individual loans, for which 80% of the losses will be borne by the State.

4.8 How long does the second guarantee scheme apply?

Initially, the guarantee scheme could be used for loans granted between the date of entry into force of the Law (24 July 2020) and 31 December 2020 for a term of 12 to 36 months. The King may, by a decree adopted after consultation in the Council of Ministers, extend this deadline and term if that is necessary owing to the severity and duration of the adverse impact of the coronavirus on the economy.

The granting period was extended until 31 December 2021 and the term to 5 years by Royal Decree of 24 December 2020, as amended by Royal Decree of 14 June 2021.

4.9 What is the impact on the allocation if banks refuse their share?

None. The second guarantee scheme is optional for banks (credit institutions under Belgian law and branches of foreign credit institutions) which had more than € 20,000 in outstanding loans and credit lines to non-financial businesses, SMEs, self-employed persons and non-profit organisations on 31 December 2019.

4.10 When will the losses be calculated ?

The total state-guaranteed credit portfolio will only be known on 1 January 2022. This portfolio may be lower than, or at most equal to, the share of the € 10 billion envelope which may be used by each bank.

The State guarantee must be called on by the last day of the month that falls one year and six months after the last possible maturity date of a guaranteed credit[1] at the latest. While the guarantee applies to individual loans, lenders should call on the guarantee for the total amount of the guaranteed loans (the portfolio) granted by that lender. This prevents an undesirable overload of guarantee claims for each individual loan. The use of the guarantee does not require that a loss on the portfolio has already been established or can be demonstrated. It only confirms that the lender expects to suffer a guaranteed loss on his portfolio. A lender calling on the State guarantee should, from that date, initiate the foreclosure of the guaranteed loans in his portfolio for which the borrower is in default. A Royal Decree will determine the manner in which the final payment is to occur and lay down the arrangements for the payment of the interim advances to which the lender is entitled.

[1] Article 15 of the Law of 20 July 2020, amended by Article 403 of the Law of 27 June 2021 on various financial provisions.

4.11 What commitment has the federal government taken on?

The State will bear 80% of a lender’s loss on a loan. The remaining 20% of the loss will continue to be borne by the lender concerned.

4.12 Which banks are covered by the second guarantee scheme?

Belgian banks and branches of foreign banks (both those from EU countries and those with their head office in a non-EU country) may call on the second guarantee scheme. Institutions which, at the end of 2019, did not have a credit portfolio for businesses, SMEs and non-profit organisations amounting to more than € 20,000 are not covered by the guarantee scheme (de minimis). This is without prejudice to the fact that those banks may be covered by the arrangements concerning payment delays for mortgage borrowers.

4.13 Which loans are covered by the second guarantee scheme?

In principle, all new additional loans and credit lines to small or medium-sized non-financial enterprises with (see questions 4.1-4.3 for definition) a term of 12 to 36 months (prolonged to five years by Royal Decree of 24 December 2020) granted by the bank between the date of entry into force of the Law (24 July 2020) and 31 December 2020 (initially prolonged to 30 June 2021 and subsequently until 31 December 2021 by Royal Decree of 24 December 2020, as amended by Royal Decree of 14 June 2021) are (optionally) eligible for the second guarantee scheme (until the bank’s share in the total € 10 billion envelope is reached).

The following credits do not fall within the scope of the guarantee scheme:

- refinancing loans which serve to repay loans granted before the date of entry into force of the Law (a loan or a part of a loan which is granted to repay a non-deselected loan covered by the first guarantee scheme and for which the lender expects that he will have to take a forbearance measure on its maturity date is not considered a refinancing loan);

- reinstatements of credits granted before the date of entry into force of the Law;

- leasing contracts;

- factoring contracts;

- consumer loans and mortgage loans which are governed by Book VII of the Code of Economic Law.

4.14 Under what conditions are refinancing loans which serve to repay loans covered by the first guarantee scheme eligible for the second guarantee scheme?

The loan covered by the first guarantee scheme (i) must have been granted to a borrower who falls within the scope of the second guarantee scheme, (ii) must not have been deselected by the lender and (iii) the lender expects that he will have to take a forbearance measure on its maturity date. This does not necessarily mean that the guaranteed loan must already be in default or in arrears. It may be sufficient that the lender, on 31 December 2021 at the latest (i.e. the expiry date of the second guarantee scheme), considers it probable that the customer will be unable to repay the loan covered by the first guarantee scheme on a maturity date and that refinancing is authorised on that basis on that date (31 December 2021) at the latest.

4.15 Does the second guarantee scheme apply to all loan products (cash loans, overdraft facilities, investment loans, documentary credits, etc.)?

All new additional loans and credit lines to all small or medium-sized non-financial enterprises (see questions 4.1-4.3 for definition) with a term of 12 to 36 months (prolonged to five years by Royal Decree of 24 December 2020) are eligible for the guarantee scheme, except for the credits mentioned in the answer to question 4.13.

4.16 Can banks request additional securities for loans that were already running on the date of entry into force of the Law?

Yes it can, provided that a proportional part of these securities, taking into account the available or outstanding principal amount of all loans concerned, is allocated to the secured loans granted by the bank to that borrower. If not, the guaranteed loss is reduced by all losses on the guaranteed loans granted by the bank to that borrower. A notable exception to this are contractual arrangements that were already in force between the bank and the borrower on the date of entry into force of the Law. These include margin calls or the conversion of mortgage mandates. In addition, the above condition does not apply to securities for new loans not covered by the guarantee scheme.

4.17 Are syndicated loans also eligible for the second guarantee scheme?

Yes, insofar the distinct credit of the participating bank in the syndicate constitutes a sufficiently differentiated engagement. That bank’s engagement is sufficiently differentiated from the engagements of the other lenders if the former engages to make a fixed maximum amount available (the “commitment”). In that case, the bank’s engagement is considered a separate credit (and only the amount made available by this bank is taken into account for the calculation of the premium and the guaranteed amount).

4.18 If there are also foreign banks in the syndicate, does the Belgian share still qualify for the guarantee?

Belgian banks in the syndicate are eligible for the guarantee for their share of the loan. The share of the banks concerned must constitute a sufficiently differentiated commitment per bank.

4.19 What about renewal of a loan/credit line already existing on the date of entry into force of the Law and expiring before the end of June 2021?

That is a reinstatement of an existing credit/existing credit line which is not covered by the guarantee scheme.

4.20 Is it possible to submit multiple applications for the same counterparty under the guarantee scheme?

It is possible to grant multiple loans under the guarantee scheme.

4.21 Can a bank give customers a new/higher credit line if they still have scope in their credit line?

Yes, the difference between the higher line (e.g. € 110,000) and the existing line (€ 100,000) is then a new loan which is eligible for the guarantee scheme. This new loan must then be structured as a separate new loan (of € 10,000, for example).

4.22 Can a customer request a new loan or credit line while still having unused scope under an existing credit line?

Yes, it is up to the bank to decide whether or not to grant it. However, the drawings on the existing credit line are not eligible for the guarantee scheme.

4.23 Can a bank refuse to grant loans or credit lines to certain customers?

Yes, in the case of new additional loans or credit lines in relation to the amount of loans and credit lines outstanding on the date of entry into force of the Law. The guarantee scheme aims at facilitating the granting of new additional credits or credit lines.

4.24 Should the maximum guaranteed principal of the guaranteed loans granted to a borrower be assessed at group level,

Should the maximum guaranteed principal of the guaranteed loans granted to a borrower be assessed at group level, and can the borrower thus borrow in excess of his liquidity need at solo level as long as this falls within the limits of the maximum guaranteed principal at group level?

Yes. The EU Temporary Framework establishes conditions and thresholds applying to the “beneficiary” of the aid, i.e. the “undertaking” to which the aid is granted. The notion of “undertaking” encompasses all entities controlled by the same natural or legal person (for further explanation see Commission Consolidated Jurisdictional Notice under Council Regulation (EC) No 139/2004 on the control of concentrations between undertakings, OJ C 95, 16.4.2008, p. 1).

For example: A, B and C form a group. A has a liquidity need of 40, B of 10 and C of 50. Thus, the maximum guaranteed principal for the group is 100.

The maximum guaranteed principal for which A can take out loans under the guarantee scheme is not limited to 40 (which is its actual liquidity need), but to 100. However, if A were to take out a loan for 60, this would limit B and C’s collective credit possibilities to 40. Naturally, the general principles of creditworthiness and the economic interest of the borrower should be taken into account.

Bijvoorbeeld: A, B en C vormen samen een groep. A heeft een liquiditeitsnood van 40, B van 10 en C van 50. De maximaal gewaarborgde hoofdsom voor de groep is dus 100.

De maximaal gewaarborgde hoofdsom waarvoor A kredieten kan afsluiten binnen de garantieregeling is niet beperkt tot 40 (wat eigenlijk haar liquiditeitsnood is), maar tot 100. Indien A een krediet zou aangaan voor 60, zal dit wel de kredietmogelijkheden van B en C samen beperken tot 40. Hierbij moet uiteraard rekening gehouden worden met de algemene principes inzake kredietwaardigheid en het economisch belang in hoofde van de kredietnemer.

4.25 What is the maximum amount that can be granted to a borrower under the second guarantee scheme?

The guaranteed principal of the guaranteed loans granted to a borrower may not exceed the highest of the following amounts, calculated at the level of the group to which the borrower belongs:

1° the borrower’s liquidity needs during a period of 18 months from the intended date of the granting of the guaranteed loan, as estimated by the borrower in a duly reasoned written statement;

2° the double of the borrower’s total annual wage costs, including social charges, in the most recently closed financial year before 1 January 2020;

3° 25 % of the borrower’s turnover in the most recently closed financial year before 1 January 2020[1]

The resulting maximum guaranteed principal should be reduced by the principals of the loans granted to the borrower (or other companies belonging to the group of the borrower) under the first guarantee scheme, insofar as they are not refinanced by loans covered by the second guarantee scheme.

[1] Article 8, §1 of the Law of 20 July 2020, amended by Article 402 of the Law of 27 June 2021 on various financial provisions.

4.25/1 Does the term "wage cost" as referred to in Article 8, § 2, 2° of the Law of 20 July 2020 also include the remuneration of the manager?

Yes, it may be taken into account insofar as it concerns a remuneration (this in contrast to payments for capital, which may not be counted).

4.26 May normal repayments of both capital and interest of loans granted before the date of entry into force of the Law be included in the simulator-based liquidity assessment ?

May normal repayments of both capital and interest of loans granted before the date of entry into force of the Law be included in the simulator-based liquidity assessment ? Are loans taken out to service these repayments covered by the State guarantee?

It should be noted that, if the loan amount is less than double the total annual wage costs, including social charges, or less than 25% of the borrower’s turnover in the most recently closed financial year before 1 January 2020, liquidity needs do not necessarily have to be taken into account for granting a loan under the second guarantee scheme.

If they are nevertheless taken into account, Article 8, § 1, 1° of the Law specifies in this regard that the relevant liquidity needs limiting the guaranteed principal do not include the borrower’s needs to repay or reinstate loans granted before the date of entry into force of the Law. However, a loan or a part of a loan which is granted to repay a non-deselected loan covered by the first guarantee scheme and for which the lender expects that he will have to take a forbearance measure on its maturity date is not considered a refinancing loan. Thus, the financing of repayments of a loan granted by the same or another lender prior to the date of entry into force of the Law qualifies in principle as a refinancing loan within the meaning of Article 3, 12° of the Law, is not eligible for the guarantee scheme and may therefore not be included in determining the liquidity needs under Article 8 of the Law. The reason is that a guaranteed loan is not intended to be used to repay an existing loan (OLD MONEY). Moreover, if the conditions of the Business Loan Charter are met, (capital) repayments are eligible for deferral of payment.

On the other hand, the lender should identify the overall liquidity needs of the borrower in order to be able to correctly assess the risks. However, the lender may include repayments of loans granted before the date of entry into force of the Law in this exercise without, however, including them in determining the liquidity needs under the (specific) framework of Article 8 of the Law. Therefore, for the purposes of determining the amounts covered by the guarantee scheme (NEW MONEY), the repayments are best treated separately in the liquidity simulator.

4.27 If the bank wants to consider delays on a due date or multiple due dates jointly on loans already outstanding on the date of entry into force of the Law and group them in the form of a new loan, is this refinancing or not?

Yes, that is refinancing which is not in principle eligible for the guarantee scheme.

4.28 Are existing loans also eligible for the second guarantee scheme?

No. The guarantee scheme does not apply to loans existing on the date of entry into force of the Law, nor to the unused amounts on credit lines existing on the date of entry into force of the Law.

4.29 Can the second guarantee scheme still be used if a customer requests a forbearance measure but the bank consequently decides to classify the customer under pre-litigation in order to monitor the case?

Yes, but only for new additional loans to that customer (in addition to loans and credit lines outstanding on the date of entry into force of the Law) or for loans which serve to refinance loans granted under the first guarantee scheme, see scope.

4.30 How does the “recovery” take place in case a guaranteed loan cannot be repaid by the customer?

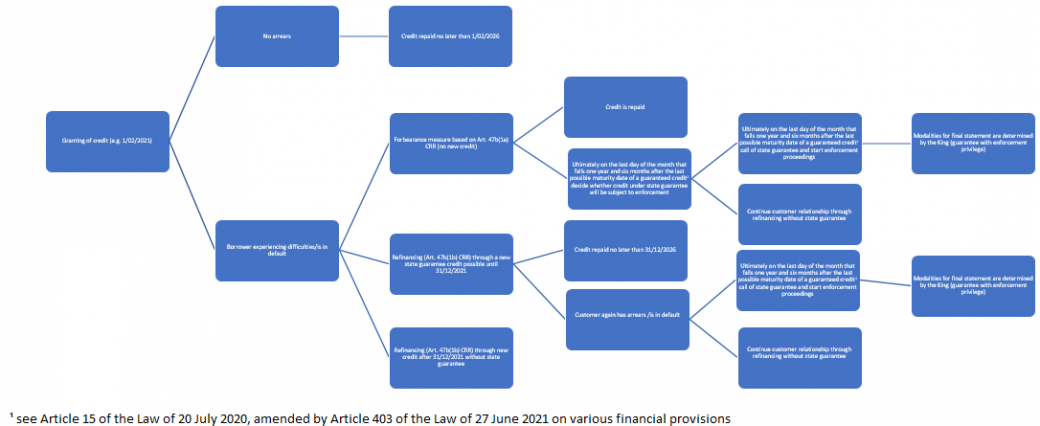

Banks must call on the State guarantee by the last day of the month that falls one year and six months after the last possible maturity date of a guaranteed credit [1] at the latest for the guaranteed loans, and this independently of the date of granting or the duration of the loan. Only then should a decision be taken as to whether or not to terminate the customer relationship. In the meantime, forbearance measures can be taken. The diagram below gives an overview of the various possibilities:

[1] Article 15 of the Law of 20 July 2020, amended by Article 403 of the Law of 27 June 2021 on various financial provisions.

4.30/1 If a forbearance measure is a deferral of payments (e.g. in the form of a repayment schedule, extension of the initial loan or otherwise) on the guaranteed loan, are the parties bound by the maximum period of the guaranteed loan (36 months under th

4.30/1 If a forbearance measure is a deferral of payments (e.g. in the form of a repayment schedule, extension of the initial loan or otherwise) on the guaranteed loan, are the parties bound by the maximum period of the guaranteed loan (36 months under the second guarantee scheme, prolonged to five years by Royal Decree of 24 December 2020)?

No, the maximum period of 36 months (prolonged to five years by Royal Decree of 24 December 2020) does not apply here. Please refer to the schedule as included in question 4.30: a forbearance measure can only be granted up to the last date on which the State can be called upon to honour the State guarantee. This last date is the last day of the month that falls one year and six months after the last possible maturity date of a guaranteed credit [1] for the second guarantee scheme.

[1] Article 15 of the Law of 20 July 2020, amended by Article 403 of the Law of 27 June 2021 on various financial provisions.

4.30/2 Is an additional premium payable by the borrower if a forbearance measure is a deferral of payments (e.g. in the form of a repayment schedule, extension of the initial loan or otherwise) on the guaranteed loan?

No. If the borrower is unable to repay the loan on the contractual maturity date, the authorised payment deferral must be regarded as a forbearance measure within the meaning of Article 47b(1)(a) of Regulation (EU) No 575/2013 and no additional premium is due. In this case, however, the requirements of Article 19, 1° Law of 20 July 2020 must be taken into account (see question 4.30/3).

4.30/3 How should the "proportionate application" of forbearance measures (taking into account the available or outstanding principal and the maturity date) be understood exactly (Article 19, 1° Law of 20 July 2020)?

“Proportionate application” means that, if a forbearance measure is granted in the form of a deferral of payments on a guaranteed loan, the other loans not covered by the State guarantee should also benefit from a payment deferral for at least the same period.

For example, if a forbearance measure is granted for a guaranteed loan, in the form of a payment deferral (e.g. repayment of a 15-month loan postponed by 6 months), all other current loans must also benefit from a deferral for the same period of at least 6 months (e.g. a 5-year investment loan must also benefit from a deferral of at least 6 months).

If there are other current loans covered by the State guarantee, the proportional payment deferral has no impact on the maintenance of the State guarantee.

4.30/4 Does the proportional application referred to in question 4.30/3 apply to any forbearance measure, including, for example, refinancing?

No. The principle of proportionality only applies to the forbearance measures referred to in Article 47b(1)(a) of Regulation (EU) No 575/2013.

4.31 When it is decided to terminate the customer relationship and to call on the guarantee, what should a bank do to ensure that the losses relating to the guaranteed loans are taken into account in calculating the State guarantee (enforcement privilege)

The bank will first have to "enforce" the customer (i.e. draw on all of the customer's funds, collateral, guarantees, etc.) before the residual amount can be considered as a loss for calculating the State guarantee. This enforcement does not have to occur or be finalised at the moment that the State guarantee is called on.

4.32 Should existing “all sums” securities always be used as guarantees for loans covered by the second guarantee scheme?

No. The lender and the borrower may, prior to or at the time of the granting of the loan covered by the second guarantee scheme (hereinafter “the guaranteed loan”), make arrangements in relation to the division of the realisation of “all sums” securities. These arrangements may in particular exclude the guaranteed loan from the proceeds of an “all sums” security, or provide that this security should be used primarily to pay loans granted before the date of the guaranteed loan and only secondarily to pay the guaranteed loan.

4.33 Can a bank transfer one or more guaranteed loans?

In principle it cannot, except as collateral for any financing granted to a bank by the National Bank of Belgium in the context of its legal mission. The collateral may relate to the loans themselves or to the securities issued by the Bank for the securitisation of these loans.

4.34 How do the different guarantees provided by the Regions and the federal State interact?

Clarification with an example:

A retail business has an outstanding loan of € 500,000 with the bank, with a total interest rate (incl. fee) of 1.5%. This is the only outstanding loan of the borrower with the bank. This loan was brought under the second guarantee scheme by the bank. When the loan was taken out, the commercial property was also included in the guarantee. The (realisable) value of the property is estimated at 150,000. If the retail business goes bankrupt, there will still be €10,000 cash in the bank and the business owns a van worth €10,000.

Case (a): no other (e.g. regional) guarantees were provided for this loan. In this case, the loss is determined by first liquidating all of the business’s assets (including the cash, the van) and by selling the trading premises. The estimated value thereof is € 170,000. The remainder of the amount (principal of the loan plus interest) € 500,000*(1 + 1.5%) - € 170,000 = € 337,500 is included in the "loss" taken into account on the basis of the first paragraph of Article 12 of the Law when applying the State guarantee to the loan in question.

Case (b): The loan also benefits from a regional guarantee (without pari passu clause) covering a loss of €100,000. In this case, the loss is determined by first liquidating all of the business's assets (including the cash, the van), and by selling the trading premises. Subsequently, the regional guarantee is called on for the full amount of the losses covered. The estimated recoverable value amounts thus to €170,000 + €100,000. The amount that cannot be recovered by the bank, namely € 500,000*(1 + 1.5%) - € 170,000 - € 100,000 = € 237,500, is included in the "loss" taken into account on the basis of the first paragraph of Article 12 of the Law when applying the State guarantee to the loan in question.

Case (c): The loan also benefits from a regional guarantee (with pari passu clause) covering a loss of €100,000. In this case, the loss is determined by first liquidating all of the business's assets (including the cash, the van) and by selling the trading premises. We assume that the pari passu qualification of the guarantee granted by the Region makes it clear that this guarantee is reduced by half as a result of the fact that the guaranteed loss of € 100,000 can also be covered within the framework of the bank's portfolio guarantee. In this case, the Region will not reimburse €100,000 on the basis of the guarantee, but only €50,000. Article 12, second paragraph of the Law stipulates that the amounts that cannot be recovered from the Regions because of the pari passu clause (in this case €50,000) will be included in the loss. The estimated recoverable value amounts thus to €170,000 + € 50,000. The remainder of the amount € 500,000*(1 + 1.5%) - € 170,000 - € 50,000 = € 287,500 is included in the "loss" taken into account on the basis of the first paragraph of Article 12 of the Law when applying the State guarantee to the loan in question.

Case d): The loan also benefits from a regional guarantee covering a loss of € 100,000 and an additional Credendo guarantee of € 50,000 (both with pari passu clause). In this case, the loss is determined by first liquidating all of the business's assets (including the cash, the van) and by selling the trading premises. We assume that the pari passu classification of the guarantees granted by the Region and Credendo make it clear in each case that these guarantees are proportionally reduced as a result of the fact that part of the guaranteed loss can also be covered within the framework of the bank's portfolio guarantee. Such pari passu arrangements involve a pro-rata allocation of the losses between the different parties. With regard to the first loss tranche of € 50,000, the pari passu clauses stipulated by the Region and Credendo have the consequence that they each reimburse a loss of only € 16,666.66. For the second loss tranche of € 50,000, the pari passu clause in the guarantee of the Region has the consequence that the Region will only pay € 25,000. Pursuant to Article 12, second paragraph of the Law, the amount that cannot be recovered from the Region or Credendo because of the pari passu clauses is included in the loss. The estimated recoverable value is thus € 170,000 + 2* € 16,666.66 + € 25,000. The remainder of the amount € 500,000*(1 + 1.5%) - € 170,000 - 2* € 16,666.66 - € 25,000 = € 279,170 is included in the "loss" taken into account on the basis of the first paragraph of Article 12 of the Law when applying the State guarantee to the loan in question.