The recovery of the Belgian economy remains stalled, even before the full adverse impact of the latest restrictions is felt

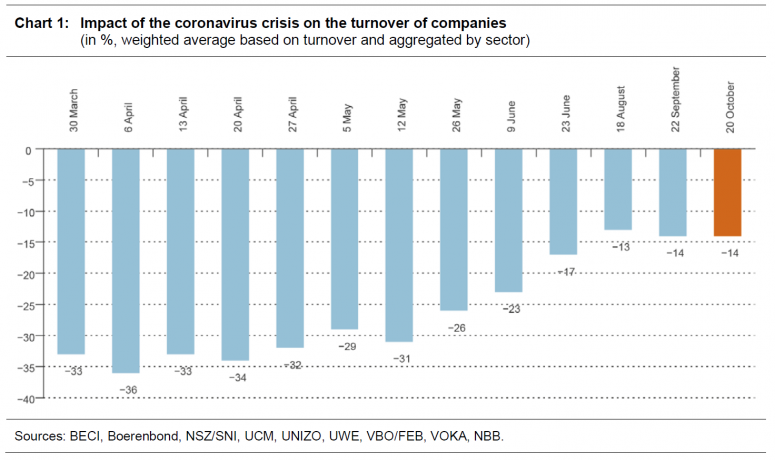

Belgian firms reckon that their turnover is 14 % lower this week on account of the coronavirus crisis, a similar percentage to that recorded in the August and September surveys. This suggests that the recovery has stalled since August. The temporary closure of bars and restaurants has led to a sharp deterioration in turnover in the accommodation and food services sector. Non-food retail shops also saw their turnover figures deteriorate in October, thus continuing the downward trend observed since the end of August. This is the main conclusion to be drawn from the latest ERMG survey among Belgian firms. Moreover, the prospects for the companies surveyed remain gloomy as they are expecting turnover to stagnate at its current level in the fourth quarter and remain 11 % below normal next year. Finally, there has been a sharp increase in the number of employees absent due to illness, notably in those sectors where teleworking is more difficult to arrange. It should be noted that this survey was carried out just after the latest federal measures for cafés and restaurants and for teleworking were announced and just before the newly adopted tighter restrictions for the leisure sector and for the Walloon and the Brussels-Capital Regions. So, these survey findings certainly do not fully reflect the impact of these latest measures.

A new survey was conducted last week by a number of federations of enterprises and the self-employed (BECI, UCM, UNIZO, UWE and VOKA). The initiative is coordinated by the NBB and the FEB/VBO. This survey follows on from a series of twelve survey rounds conducted since March, with the aim of assessing the impact of the coronavirus crisis and the lockdown measures on economic activity in Belgium and on the financial health of Belgian companies. The survey has been conducted on a monthly basis since August. In all, 5 131 companies and self-employed people responded to this week’s survey[1]. Changes in the indicators cited should be interpreted with caution. Owing to the time span between the surveys, a “survival bias” may appear, particularly in the worst-affected sectors. It is possible that some companies in difficulty have meanwhile filed for bankruptcy and as a result no longer take part in the survey. Moreover, the federations and companies taking part in the initiative may differ from one survey to the next.

The survey was carried out on 19, 20 and 21 October, which was just after the entry into force of the federal measures concerning teleworking and the closure of bars and restaurants for a period of four weeks. After the survey, additional restrictions were also introduced, notably for the leisure sector and in the Walloon and Brussels-Capital Regions. The impact of all these measures is not yet reflected, at least not fully, in the results of this survey. It is therefore very likely that the economic situation in Belgium is still being over-estimated in the findings and the situation is actually getting worse rather than stagnating.

Company turnover remains well below its pre-crisis level

Taking account of company size and sectoral value added, firms questioned this week reported that their revenue is now 14 % lower than normal. This figure is in line with the August and September figures (respectively -13 % and - 14 %). At regional level, the impact of the coronavirus crisis continues to be perceived as being lower in Flanders. The bigger impact in the Brussels-Capital Region is above all related to the drop in the number of commuters, tourists and business trips and it is mostly evident in accommodation and food services, retail trade and the transport and logistics sector. In the Walloon Region, support services are affected more than in the other two Regions.

[1] Participation in the survey by some federations whose members are part of a specific sector of activity may lead to a sampling error. In particular, companies from one by branch of activity could be more strongly represented in our sample than in the Belgian economy as a whole. The sample is therefore stratified by industry based on the weight in value added in Belgium. It should also be noted that the figures may differ slightly from previous publication figures due to the inclusion of data received afterwards and because the data analysis is constantly being refined.

The fact that there has been no further improvement over a period of two months is largely due to the persistent weakness of demand (which once again explains the current revenue loss for more than half the firms surveyed), and the recent increase in the number of COVID-19 infections and the tightening of the restrictions. First of all, owing to the closure of cafés and restaurants, the share of firms questioned that cited the total or partial prohibition of activities as a reason for the current turnover loss has risen from 8 % in September to 12 % in October. That said, this rate is still well below the 25 % recorded during the lockdown in March-April, when, among other measures, almost all non-food shops were closed. Secondly, the number of companies citing a lack of staff as one of the reasons behind the fall in turnover has more than doubled, rising from 2 % in August to 3 % in September and, finally, to as much as 5 % in October.

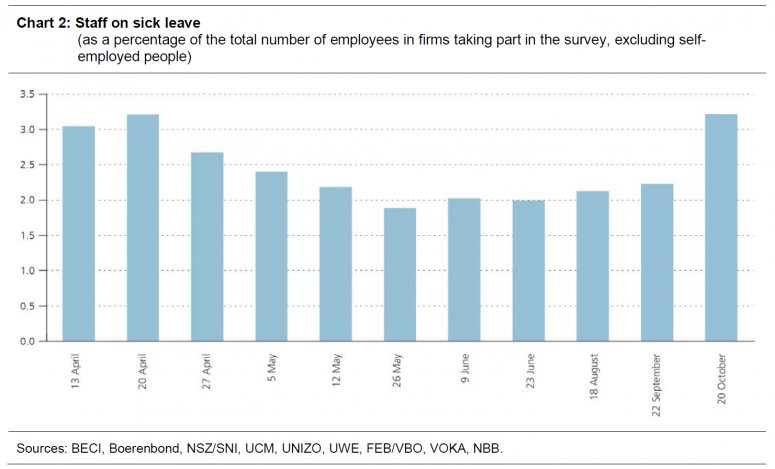

This is also confirmed by the increase in the proportion of employees off sick, which has risen from 2.2 % in September to 3.2 % in October, a similar level to that recorded in mid-April. Of course, that cannot be dissociated from the growing number of COVID-19 infections and, consequently, people in quarantine. This percentage of workers absent owing to illness is much higher in the Brussels-Capital Region (3.8 %) and the Walloon Region (4.3 %) than in the Flemish Region (2.6 %), as in sectors where teleworking is more difficult to arrange, like agriculture (8 %), industry (5 %), transport and logistics (5 %) and construction (4 %).

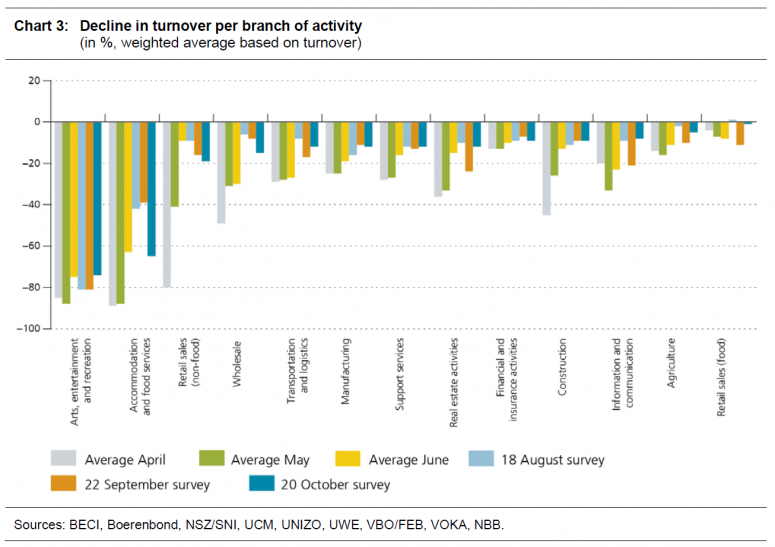

The current revenue loss in the accommodation and food services sector was up considerably in the October survey, to reach 65 %. This is probably still an under-estimate of the real situation because the survey was conducted just after the new decision to close restaurants and cafés at national level, the impact of which was perhaps not entirely taken into account by then. The accommodation and food services sector was already among the worst hit in the Spring lockdown and suffered an average drop in turnover of more than 85 % from mid-March to the beginning of June, which was then only brought back to still 40 % in August and September, owing to the social distancing measures and weak demand.

Firms in the non-food retail sector – which had been among the worst affected during the spring lockdown – have seen the impact of the coronavirus crisis on their turnover deteriorate over the last two months: -9 % in August, -16 % in September and -19 % in October. Businesses in this sector are among the most sensitive to changes in the health situation notably due to the negative correlation with shop visits, related to the fear of catching the virus or the inconvenience of the restrictive measures. Besides, this sector will also be adversely affected by the closure of cafés and restaurants, because shopping trips and catering visits are often combined. Companies in food retailing, on the other hand, have only reported a limited impact of the coronavirus crisis on their turnover in October (the closure of restaurants could have had a positive influence).

For most of the other sectors of activity, the revenue loss remains generally comparable to those of the two previous the surveys. Firms questioned in the arts, entertainment and recreation sector in October have again reported a very significant loss of turnover compared to a normal situation (-74 %), and this percentage is expected to get worse following the measures taken recently for this sector. The accumulation of such poor results in this sector for more than seven months risks having dramatic consequences. In the case of construction, support services, transport and logistics and the manufacturing industry, relative stability is noted in comparison with the two previous surveys.

Lastly, an improvement in turnover is noted for agriculture, real estate activities and the information and communication sector. These results should nevertheless be interpreted with caution as these three sectors of activity posted highly volatile results in the last few surveys and because the sample is small for agriculture and real estate activities. Without these three sectors, the overall turnover loss would have been worse in October.

When questioned about the impact of the coronavirus crisis on turnover in the fourth quarter of 2020, firms surveyed said they were expecting a similar situation to the current loss of turnover, or even worse for non-food retailing. For 2021, companies questioned are predicting hardly any improvement at all: their projections point to an 11 % turnover loss, which is slightly worse than had been expected in the previous survey. The worst hit sectors at the moment are only expecting a partial reduction in their losses in 2021, and not one single sector is expecting any improvement on the norm.

The degree of concern about the firm’s commercial activity, measured on a scale of 1 (low concern) to 10 (high concern), has risen from 6.4 in September to 7.0 in October, a similar level to that recorded in April. The growing concern among firms, the gloomy outlook for turnover and the huge uncertainty could be detrimental for investment. Regarding 2020, firms surveyed mentioned a 23 % reduction in investment compared with the normal situation and investment plans for 2021 are estimated to be 21 % below normal. This is a slight deterioration of 2 percentage points on the previous survey.

Almost one in every two firms could only survive a second lockdown with support measures

The proportion of firms surveyed saying that bankruptcy is either likely or very likely reached 8.1 % this week. This figure is similar to the August numbers. In September, the perceived bankruptcy risk was lower, but that stems from the fact that small firms based in Wallonia and Brussels, which regard the risk of bankruptcy as higher, were much less represented in that survey. Besides, it is possible that some companies in difficulty have meanwhile filed for bankruptcy and have therefore stopped taking part in this survey (what is referred to as ‘‘the survival bias’’). By way of example, firms surveyed reckon that up to 8 % of companies operating in their own sector of activity have already filed for bankruptcy or are currently involved in bankruptcy proceedings because of the coronavirus crisis. The fact that companies in liquidation no longer take part in the survey means that the adverse impact of the coronavirus crisis is possibly under-estimated.

An additional question about the impact of a hypothetical second lockdown of six weeks on the risk of bankruptcy was added to this week’s questionnaire. 5 % of the firms surveyed felt that another lockdown of this kind would push their business over the edge even if the financial support measures put in place during the Spring lockdown are rolled over. For 45 % of respondents, the very survival of their firm is directly dependent on the financial support measures and, if they are not applied as they were during the Spring lockdown, bankruptcy would be inevitable. Dependence on financial aid in the event of a hypothetical lockdown is particularly high for firms in accommodation and food services, the arts, entertainment and recreation sector and non-food retailing as the survival of almost eight out of ten firms in these sectors would depend directly on these measures.

As far as liquidity-related aspects are concerned, companies surveyed also pointed to a deterioration on the previous month. In the October survey, 32 % of the firms questioned said they had liquidity problems, compared with 25 % in September and 30 % in August. In order to gauge companies’ liquidity position, they were also asked for how long they could meet their current financial liabilities without having to rely on additional capital injection or loans. The answer was less than one month for 3 % of the respondents and between one and three months for 19 % of the respondents, which means that almost one in every four firms is now in precarious financial situation.

Nor are there any signs of recovery in terms of forecasts and prospects for employment in the private sector. Based on answers from firms taking part in this survey, employment in the private sector is expected to fall by almost 90 000 employees in 2020 (or a 3.6 % drop in employment in the private sector) and by nearly 15 000 employees in 2021 (or a 0.6 % drop in employment in the private sector). In the October survey, companies said 7 % of their employees are now on temporary lay-off, compared with 6 % in September. This increase is entirely attributable to the rise in temporary lay-offs in the accommodation and food services sector, which shot up from 34 % in September to 60 % in October, and this percentage is probably largely under-estimated because it does not fully reflect the impact of the recent national lockdown.

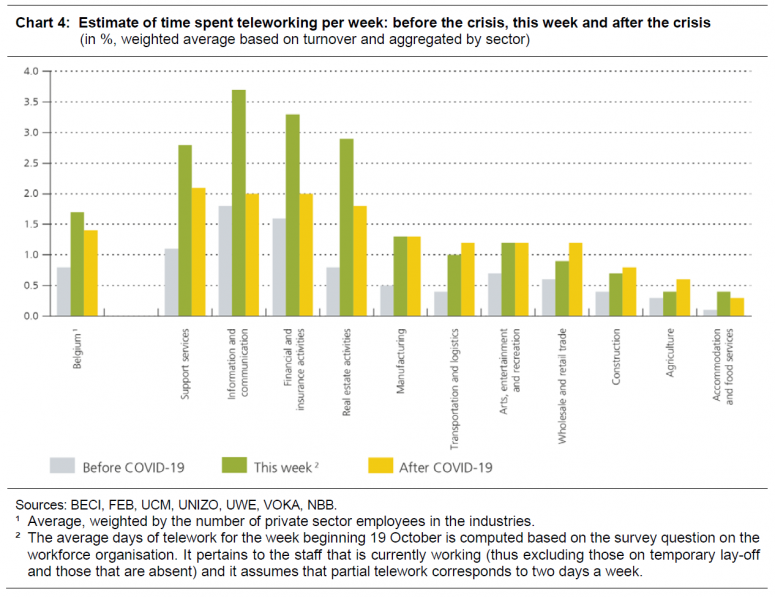

The use of teleworking is once again rising sharply and is likely to double in frequency after the crisis

This week, ways of working have also changed as full-time teleworking is once again the general rule in companies where working from home is possible. As a result, the share of full-time teleworking has risen sharply, from 9 % in September to 22 % in October, while the proportion of part-time teleworking is also still high (22 %, compared with 26 % in September). Moreover, these figures probably do not yet fully reflect the impact of the recent measures.

Even after the coronavirus crisis, companies are expecting more intensive use of teleworking than before the crisis: the average number of days spent working from home per week is projected to rise from 0.8 to 1.4 days. This is only slightly down on the current figure of 1.7 days teleworking a week. In particular, support services, the information and communication sector, financial and insurance activities will in future make wider use of working from home, with an average of two days a week.