The National Bank estimates the impact of the Trade Agreement between the EU and the United Kingdom on Belgian GDP at 0.4 of a percentage point over the next five years

NBB Communication on the economic impact of the Trade and Cooperation Agreement (TCA) between the EU and the United Kingdom

Brexit, a theme followed closely by the Bank

Ever since the British referendum on Brexit in June 2016, the Bank has regularly published papers not just on the economic implications of this choice made by the United Kingdom’s citizens, but also on financial matters, notably in its capacity as a supervisory authority. The Bank has also co-chaired the Brexit Task Force within the International Relations Committee of the European System of Central Banks. It was this Task Force that was behind the publication of an ECB Occasional Paper covering many different aspects of the economic dimension of Brexit at European level.

The 24 December deal: objectives of this Communication

The United Kingdom officially left the EU at the end of January 2020. Throughout the last eleven months of the transition period, relations between the United Kingdom and the EU continued to be governed by legislation in force in the EU (the acquis communautaire). On 1 January 2021, Great Britain left the Customs Union and the Single Market, while Northern Ireland de facto remains in it. But while the risk of a no-deal Brexit was looming large, on 24 December 2020, the British Government and the President of the European Commission concluded a Trade and Cooperation Agreement which came into force provisionally at the beginning of the year.

In this Communication, we are providing the public with some information about the impact of Brexit with this type of deal, as well as what the new Agreement brings in terms of advantages over a no-deal situation.

What is in the economic side of the deal?

From a purely trade point of view, it is a free trade agreement with neither customs duties nor quotas on all goods, with the exception of those with only very little content produced in the EU or in the United Kingdom. The TCA also provides for wide market opening, especially for public procurement, transport and energy, including nuclear power. With a view to ensuring free and fair competition, les deux parties have undertaken to maintain high levels of protection for labour, social protection, the environment and climate as well as common principles for state aid. TCA commitments in terms of services are relatively limited. Financial services, for instance, are dependent on the equivalence decisions that are taken (unilaterally) by both parties. This type of services and other aspects could nevertheless be covered in more detail by future agreements.

Taking account of the existing close economic integration between the United Kingdom and the EU and their geographical proximity, the TCA will, to some extent, go a bit further than existing agreements between the EU and other countries, including those concluded or implemented only recently, both in terms of market access and alignment. However, non-tariff barriers, notably customs formalities, animal and plant health checks, respect for norms and standards that may evolve differently in the two geographical areas, will therefore be reintroduced, effectively pushing up the cost of trade between the two parties.

In a bid to limit the short-term economic damage, a five-and-a-half-year transition period has been agreed for the thorny issue of fisheries. In addition, the mist badly affected countries in the EU, including Belgium, will benefit more from the Brexit adjustment reserve of €5 billion (at 2018 prices) managed by the European Commission, the bulk of which will be made available for the Member States in 2021.

What is the economic impact for Belgium of a Brexit deal and the Agreement itself?

Economic Brexit has effectively put an end to free movement of goods, services, people, and to a lesser extent, capital. As far as trade is concerned, the end result will be non-tariff barriers, costs for trade between Great Britain and the EU, a reduction in the volume of trade and a loss of GDP.

For all countries, the agreement nevertheless helps to limit the loss compared with a no-deal scenario where trade would only have been subject to World Trade Organisation (WTO) rules and, in particular, the most-favoured nation clause.

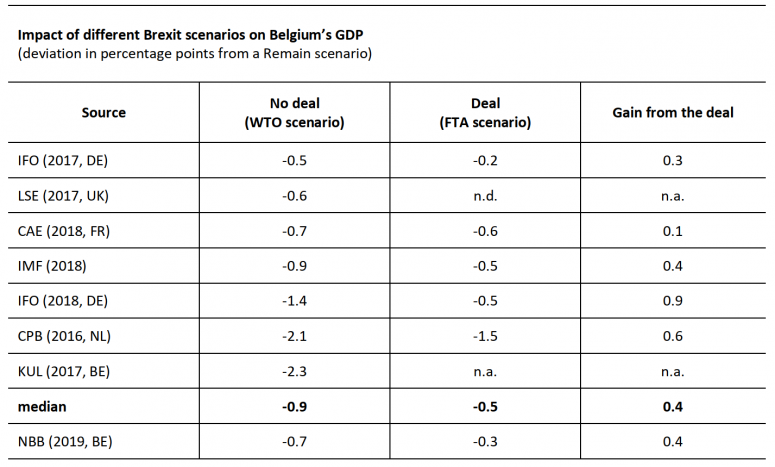

For Belgium, in the long term, compared with a scenario where trade is subject to Customs Union and Single Market rules (Remain scenario in force until the end of December 2020), the median economic loss among the studies reviewed in January 2019 was 0.9 of a percentage point of GDP in a no-deal (WTO) scenario and half a percentage point in a CETA-type free trade agreement scenario (EU-Canada Agreement).

Sources: Bisciari P. (2019), A survey of the long-term impact of Brexit on the UK and the EU27 economies (repec.org), NBB WP 366; NBB.

FTA = CETA-type free trade agreement; WTO = World Trade Organisation.

The CPB estimates refer to Belgium and Luxembourg. In the FTA scenario, it is assumed that the free trade agreement only comes into force in 2029, that is, one year before the end of the projection period.

The NBB’s estimates give the cumulative impact on GDP over five years after the transition period.

To recap, the estimates carry a high degree of uncertainty as this is the first time that a Member State has left the EU. Reflecting this uncertainty, estimates vary between 0.5 and 2.3 percentage points of GDP for a WTO scenario and between 0.2 and 1.5 percentage points for a free trade agreement scenario. Moreover, these studies only focused on the trade channel. In the case of fisheries, tariff and non-tariff barriers are included but access to British waters is not. And lastly, these are estimates on the basis of unchanged policy. Yet, the British voted for Brexit to get back their autonomy and thus change their policies; so the EU countries may also react in a bid to limit any losses.

In Box 9 of the Annual Report 2019, an estimate made from the Bank’s macroeconometric model put the loss of economic activity over a five-year horizon at 0.3 of a percentage point of GDP in a free trade agreement scenario and 0.7 of a percentage point in the WTO scenario, compared with a Remain scenario.

Compared with a no-deal scenario, as used in the Bank’s latest macroeconomic projections (December 2020), the new Agreement should therefore lead to a 0.4 percentage point increase in the level of economic activity by the year 2025, with most of this growth concentrated in the years 2021 and 2022. To recap, in December, the Bank was predicting a growth rate of 3.5 % in 2021 and 3.1 % in 2022.