Loss of turnover due to coronavirus crisis still high although already reduced by half

Brussels, June 2020 – Belgian firms reckon that their turnover is still 17 % below pre-crisis levels, which is only about half the impact declared during the weeks in lockdown. This amounts to a recovery of six percentage points in the space of two weeks and nine percentage points in the space of a month. The recovery is fairly widespread across sectors and this week it concerns catering and accommodation in particular, where turnover has picked up considerably, despite not yet being back to half of its pre-crisis level. Perception of the risk of bankruptcy, liquidity problems and the degree of concern have also improved. These are the main findings of the tenth ERMG survey among Belgian firms. Although these indicators appear to be getting gradually better, the impact of the crisis on businesses is nevertheless still significant. Besides, the outlook for investment and employment remains bleak. A full recovery will take time.

A new survey was conducted last week by a number of federations of enterprises and the self-employed (notably, BECI, SNI, UNIZO, UWE and VOKA for this latest survey). It is the tenth of its kind to be held since the end of March. This initiative coordinated by the NBB and the FEB/VBO aims to assess the impact of the coronavirus crisis on economic activity in Belgium and on the financial health and decision-making of Belgian companies. A total of 3 136 companies and self-employed people responded to this survey[1]. This series of polls has now been suspended until further notice. In principle, no further surveys will be held in either July or August.

[1] Participation in the survey by some federations whose members operate in a specific sector of activity may lead to a sampling error. In particular, companies from one by branch of activity could be more strongly represented in our sample than in the Belgian economy as a whole. The sample is therefore stratified by industry based on the weight in value added in Belgium. Note that the changes over the weeks should be interpreted with caution, as the companies that reply to the survey are not necessarily the same each week.

Company turnover continues to improve and appears to be relatively widespread across sectors

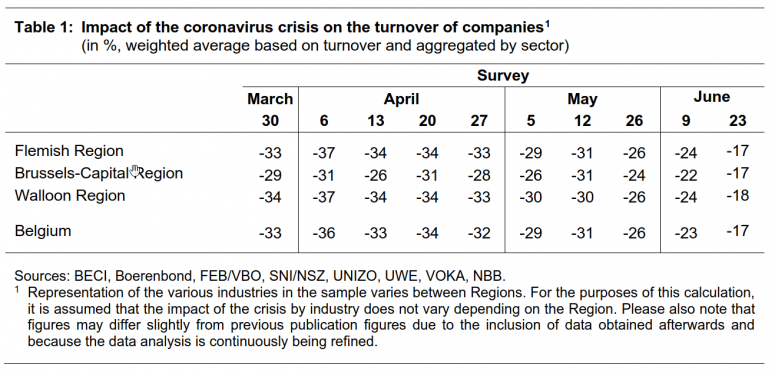

Taking account of company size and sectoral value added, firms questioned this week reported a 17 % drop in their turnover from the pre-crisis period. This is an improvement of 6 percentage points on the previous survey carried out two weeks ago and 9 percentage points on last month. Moreover, the loss of turnover has been reduced by half in comparison with the surveys conducted during the lockdown period (from 30 March to 27 April). Although these figures are somewhat encouraging and reflect the positive impact of the different phases of deconfinement, they suggest that the full recovery from the loss of sales will take some time.

For most sectors, turnover losses have contracted sharply in comparison with the lockdown period. A marked improvement has notably been observed among surveyed firms active in non-food retail sales (+74 percentage points), construction (+40 percentage points), catering and accommodation (+38 percentage points), wholesale trade (+25 percentage points), support services (+15 percentage points), real estate services (+15 percentage points) and manufacturing (+8 percentage points). Whereas two weeks ago, the improvement was particularly strong in the sectors that had suffered a bigger drop in their turnover during the lockdown, this week, the marked improvement is also visible in other sectors whose activity had initially been less directly affected by the lockdown, such as support services, manufacturing and information and communication services. On the other hand, companies in the transport and storage sector as well as agriculture have not reported any such progress over the last few weeks.

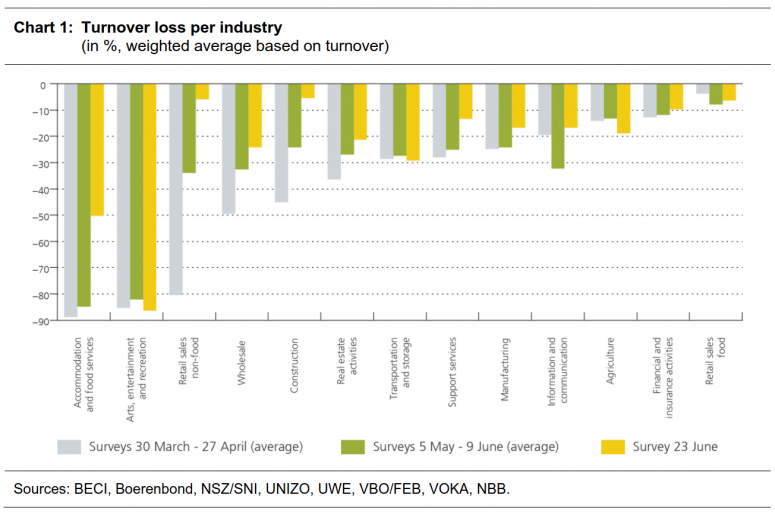

Not surprisingly, catering and accommodation is one of the sectors where the situation has improved the most sharply over the last two waves of the survey. The drop in turnover reported by companies surveyed in this this sector compared with the pre-crisis situation has thus fallen back from 85 % at the end of May to 75 % at the beginning of June and to 50 % this week. The resumption of certain business activities naturally explains this positive trend. Despite the marked improvement in its turnover, catering and accommodation is currently still the second hardest-hit sector after the arts, entertainment and recreation sector. This week, firms questioned from this latter sector in fact reported turnover as still being 86 % below its pre-crisis level. The average drop in turnover in this sector over the different survey rounds is 84 % and companies from the sector have therefore had to endure more than three months in this situation.

As far as the third quarter of the year is concerned, at this stage, eight out of every ten firms questioned are not expecting to get back to the same level of turnover in the July-September period as that recorded before the crisis. In the case of almost all the sectors surveyed, insufficient demand is still by far the biggest obstacle to a full recovery of turnover: this is cited by almost six firms out of every ten questioned. For some sectors, the hygiene and social distancing measures, the prohibition of certain activities and supply chain problems are also perceived as major constraints. On the other hand, staff shortages and liquidity problems are not often mentioned as being obstacles to a recovery of turnover.

The number of companies signalling a high risk of bankruptcy has dropped considerably

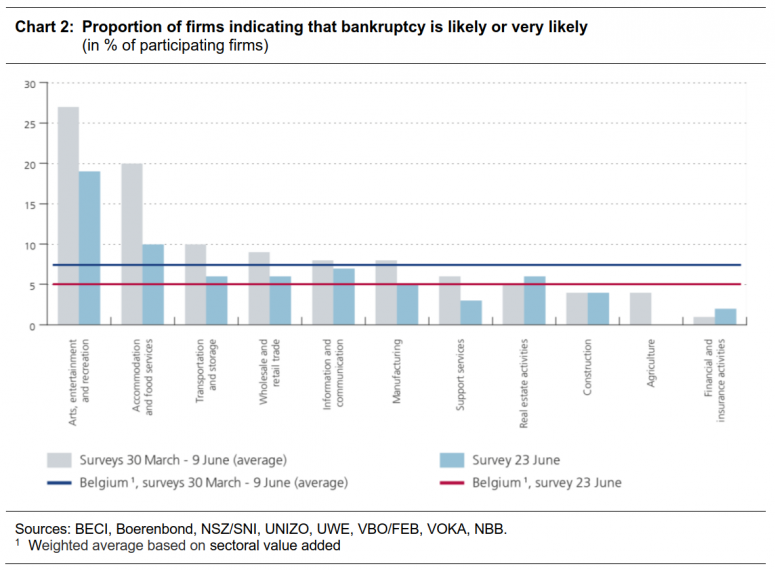

Businesses surveyed during this latest survey also appeared less pessimistic about the risk of bankruptcy: this week, only 5 % of the respondents reported that bankruptcy was either likely or very likely. By way of comparison, the figure was 6 % two weeks ago and even 8 % a month ago. It is among the surveyed firms from the catering and accommodation sector that the improvement has been the sharpest (down from 23 % in the previous survey to 10 % in this survey). However, the risk of bankruptcy within this sector is still twice as high as the national average.

Companies’ liquidity positions have also further improved according to the findings of this latest survey. In fact, only one in five businesses now say they are not able to maintain their liquidity position for more than three months. By way of comparison, this concerned 38 % of enterprises during the lockdown and 23 % in the previous survey in the previous survey. More specifically, for respondents from the catering and accommodation sector, the figure has fallen back from 46 % in the previous survey to 36 % this week.

Moreover, the degree of concern, measured on a scale of 1 (unconcerned) to 10 (very concerned), has fallen again this week, thus continuing the downward trend observed since the first phase of deconfinement dating back to the beginning of May. Since the previous survey, the index has thus come back down from 6.3 in the previous survey to 5.9 this week. When it comes to investment plans, companies nevertheless continue to exercise caution since the estimate of the impact of the coronavirus crisis on investment has remained stable, on average, compared with the previous survey. Companies that had investment plans predict an (unweighted) average drop in their investment of 34 % compared with what they had anticipated before the coronavirus crisis. This figure was 32 % in the previous survey. If this decline were to materialise, it would have a clear impact on domestic demand and, a fortiori, on economic growth.

While the number of workers on temporary lay-off has dropped sharply, forecast job losses are still high

In many respects, this week’s results appear to be better than those recorded during the lockdown weeks. One other notable positive element contributing to this improvement lies in the big decline in recourse to temporary layoffs since the end of April, a decline confirmed survey after survey. At the end of April, the firms questioned said temporary lay-offs concerned 29 % of employment in the private sector (excluding the self-employed). This week, the proportion of temporary lay-offs in the private sector has fallen back to ‘‘only’’ 11 %. Moreover, this downward trend is especially clear in the catering and accommodation sector, which has seen the share of its employees on temporary lay-off plummet from 89 % at the end of May to 38 % this week.

The labour market situation nevertheless remains worrying as, on the one hand, the rate of 11 % of private sector jobs put on temporary lay-offs is still high (and a heavy financial burden) and, on the other hand, the employment prospects for the coming months are still shrouded in pessimism. More precisely, one of the survey questions concerns the outlook for employment in firms between now and the end of the year and this week’s results suggest an estimated reduction in the number of employees in the private sector of around 6 %, i.e. more than 150 000 people. Even though that is quite some improvement on the reduction of 180 000 employees estimated on the basis of survey findings at the beginning of June, this negative impact on the labour market remains substantial. Besides, the percentage reduction in the number of employees is expected to be even bigger in certain sectors like catering and accommodation (-15 %) and the arts, entertainment and recreation (-32 %).