The direct economic impact of the second lockdown is limited for the moment, but the outlook for Belgian firms remains bleak

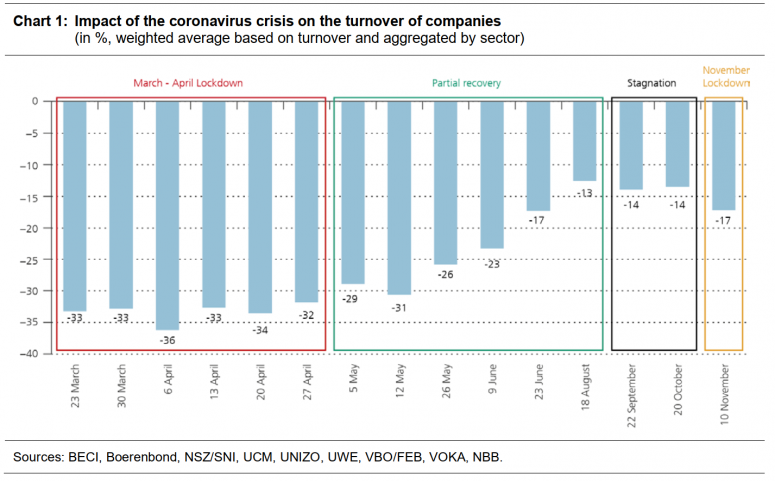

The loss of turnover incurred by Belgian firms as a result of the coronavirus crisis has risen to 17 % in November. This is 3 percentage points down on the period running from August to October but roughly half the huge loss of revenue recorded during the first lockdown in March and April. This is the main conclusion to be drawn from the latest ERMG survey among Belgian firms. The second lockdown is mainly affecting sales turnover in the accommodation and food services sector, retail and wholesale trade and real estate activities, but the impact there is still lower than during the first lockdown. In addition, no deterioration of turnover has been reported in the other industries in November, although many of them had been badly hit during the first lockdown. All the same, the outlook has got gloomier for turnover in 2021, for investment plans, employment and the risk of bankruptcy. The coronavirus crisis is also leading to a structural increase in e-commerce.

A new survey was conducted last week by several federations of enterprises and self-employed people (BECI, NSZ/SNI, UCM, UNIZO, UWE and VOKA). The initiative is coordinated by the NBB and the FEB/VBO. This latest opinion poll is the fifteenth round of a survey conducted since March, with the aim of assessing the impact of the coronavirus crisis and the lockdown restrictions on economic activity in Belgium and on the financial health of Belgian companies. In total, 5 631 companies and self-employed people responded to this week’s survey.

The ERMG survey is based on assessments given by the companies taking part in it, so the results should be interpreted with caution. Firms questioned vary from one survey to the next, given that, on the one hand, the federations running the questionnaires among their members are not necessarily the same and, on the other hand, all firms do not systematically take part in each survey. This makes comparison over time difficult. Although we correct for any over-representation in the sample of firms from certain sectors, it is possible that the firms polled differ over time in terms of other characteristics. For instance, a “survival bias” may appear owing to the time lag between surveys, some companies in difficulty are meanwhile likely to have filed for bankruptcy and no longer take part in the new survey. Moreover, this week’s survey includes more smaller firms than the previous one, but that is of less importance for the indicators for which a weighted average is calculated on the basis of turnover or the number of employees in the firms.

The effect of the coronavirus crisis on turnover is twice as weak as during the first lockdown

Taking account of company size and sectoral value added, firms questioned this week reported that their revenue was now 17 % lower than normal. This is a deterioration of 3 percentage points on the period running from August to October and which accounts for roughly half the huge loss of turnover recorded during the Spring lockdown. The gap in terms of impact on turnover between the Regions has narrowed since the previous survey, even though Brussels is still the most heavily impacted Region. And lastly, the current lockdown is once again affecting the self-employed and small firms more heavily.

The sectors of activity that were the most badly affected in the spring once again report a very negative impact, although much smaller, on their turnover. They include non-food retailing, real estate activities, accommodation and food services and the arts, entertainment and recreation sectors. These sectors are obviously considerably affected by the total or partial ban on their business activities, which is cited by more than two-thirds of companies questioned from these sectors as a major reason for their loss of turnover.

The loss of non-food retail sales turnover has deteriorated sharply since the summer, rising from 9 % in August and 19 % in October to 51 % today. The net decline registered in November is mainly due to the compulsory physical closure of non-essential shops. The impact of the current lockdown is nevertheless lot smaller than the 80 % loss of turnover observed during the first lockdown. This can be mainly explained by the fact that a much greater number of shops are now allowed to remain open and on-line sales and in-shop collection services have become much more widely used sales channels. The slightly higher loss of turnover in food retailing compared with last spring is partly attributable to the ban on sales of certain non-essential products. More generally, large firms seem to be under-represented in the sample for this sector in this latest survey, as well as in previous waves, so the loss of revenue in this sector is likely to be lower than the average for the survey. Moreover, reflecting the decline in retail trade, the loss of sales revenue in wholesale trade has also risen, to 19 % of normal levels.

The loss of turnover in the real estate activities sector has also deteriorated sharply in November, rising from 12 % in October to 37 % this month. This can possibly be explained by the tight restrictions on physical viewings for property sales or rentals. Lastly, the arts, entertainment and recreation sector and accommodation and food services are still the most badly hit sectors. Their loss of turnover has reached respectively 77 and 66 %, the same levels as observed in the October survey, which took place just after the closure of bars and restaurants. In both these sectors, this loss of turnover has nevertheless been less heavy than in the spring (especially in the accommodation and food services sector), which may be due to more intensive use of online sales and orders.

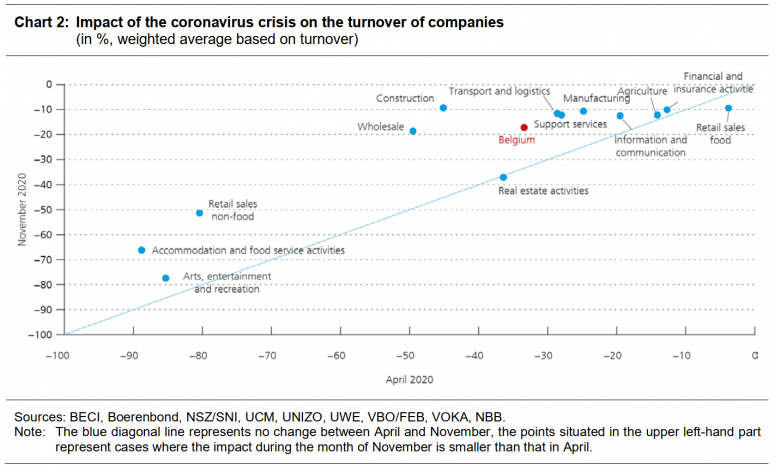

Turnover in other sectors has not seen any drastic drop in November. Among industry, construction, support services, the transport and logistics sector, financial and insurance activities (a group of sectors that account for more than 70 % of value added of the sectors taken into account in this survey), the reported drop in turnover caused by the coronavirus crisis is similar to that recorded in October and below that observed during the first lockdown. For these sectors, weak demand is still the key determining factor of the impact of the coronavirus crisis on turnover. The scale of foreign demand depends on the type of business activities and is more pronounced in industry and transport and logistics, for example. In November, firms questioned in both these sectors reported a 10 % fall in sales abroad compared with normal levels, which is a slight improvement on the previous survey (-12 % for both sectors) and a similar figure to total revenue loss in this sector.

The outlook in terms of company turnover has darkened for the current quarter and the coming year. More precisely, firms questioned are expecting their revenue to be some 16 % lower than normal in the fourth quarter of 2020. In 2021, according to the companies surveyed, turnover is expected to pick up again only very modestly and, on average, is likely to remain 12 % below normal, an estimate that is only very slightly worse than those from the two previous surveys.

Firms are also predicting less favourable employment and investment levels in 2021

The degree of concern about the firm’s current commercial activity, measured on a scale of 1 (low concern) to 10 (high concern), has remained more or less constant in November, at 6.9, a level comparable to the very high degree of concern reached during the first lockdown. The serious concern among firms, the deterioration of turnover figures and the heightened uncertainty about the way the health situation is developing all have a negative impact on companies’ investment plans. The firms surveyed are expecting the coronavirus crisis to depress investment by 25 % in 2020, compared to normal levels, and by 23 % in 2021. So, investment is only likely to pick up very modestly between these two years. It is also worth noting that investment prospects for 2021 have got slightly worse since September (-19 % in September, -21 % in October and -23 % in November).

The outlook is also gloomy for private sector employment. While estimates of job losses have improved marginally for 2020 (down from 89 000 units in the October survey to 84 000 units in the November survey), employment is expected to contract by almost 60 000 units in the private sector in 2021. This is significantly worse than the estimates based on survey replies from the month of October, which had suggested a reduction of 15 000 units. This downward trend is observed in almost all sectors of activity and is probably the result of a combination of the extension of the temporary lay-off scheme and the darkening outlook for the economy.

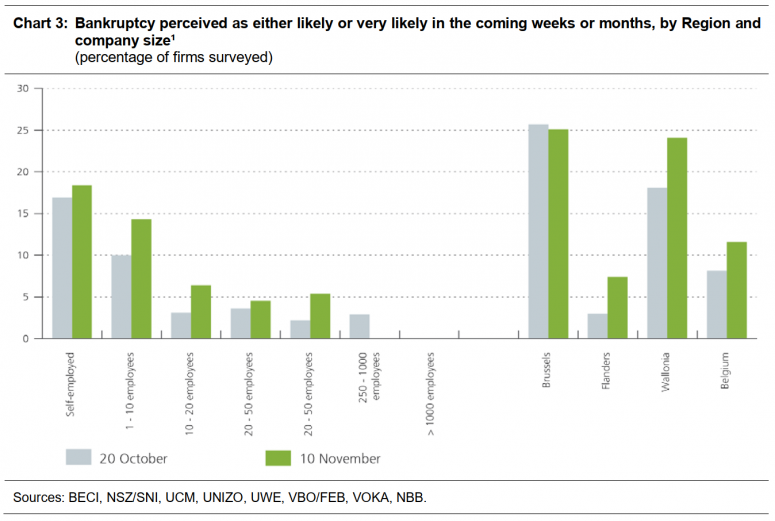

The risk of bankruptcy has risen, especially among small firms

The further loss of revenue after an only partial recovery and the gloomier economic prospects are two factors that tend to raise the risk of a company collapsing. In the November survey, the share of enterprises considering that bankruptcy is either likely or very likely in the coming weeks or months has risen from last month. The upward trend in the risk of bankruptcy is a reality in both Wallonia and Flanders (for Brussels, the indicator has stabilised after a sharp rise in October) and among the self-employed and small and medium-sized enterprises (up to 250 employees). In terms of level, however, differences continue to be observed and the self-employed and small enterprises as well as Walloon and Brussels-based firms point up the highest risk of bankruptcy. It should also be noted that the sectors facing a higher-than-average risk of bankruptcy are accommodation and food services (29 %), arts, entertainment and recreation (28 %), transport and logistics (20 %) and non-food retail trade (17 %). In the case of these four sectors of activity, the indicator rose between October and November.

At aggregate level, the proportion of firms surveyed mentioning that bankruptcy was either likely or very likely in the coming weeks or months has risen from 8 % in October to 12 % in November. However, the increase in the risk of bankruptcy may be partly attributed to the higher share of small firms in November’s sample. These enterprises are ostensibly confronted with a higher risk of bankruptcy in the coronavirus pandemic context.

The perception of a greater risk of bankruptcy is confirmed by the replies to other questions posed in the survey regarding the risk of bankruptcy. On the one hand, in response to the question “Has your company been declared bankrupt or has it already filed for bankruptcy?”, 8 % of companies said they were currently involved in bankruptcy proceedings or would be starting them over the next six months, compared with just 5 % in October. On the other hand, the firms questioned consider that 11 % of companies operating in their own sector of activity have already filed for bankruptcy or are currently involved in bankruptcy proceedings, compared with 8 % in October. The different questions bring additional information and are therefore not entirely comparable, but the common thread is the upward trend in the perceived risk of bankruptcy.

As regards liquidity problems too, a worsening of the situation is reported in the November survey. The share of firms surveyed pointing to cash-flow problems has gone up from 32 % in October to 35 % in November. Some deterioration is also observed among responses to the question ‘‘For how long can your company meet its current financial liabilities without having to draw on own funds or new loans?’’. While in October, 23 % of firms surveyed said they could cope for three months at most, this percentage is up to 27 % in November. Between October and November, the liquidity position has deteriorated sharply in the non-food retail sector and the transport and logistics sector.

Recourse to temporary lay-offs is rising but is still well below April levels

One of the support measures announced on 6 November was the reintroduction of temporary lay-offs on grounds of force majeure for all companies. According to the November survey, 11 % of private sector employees were on temporary lay-off, against 6 % in September and 7 % in October. At the current juncture, this is in strong contrast to the 32 % reported by firms at the beginning of April, which is another indication that the direct impact of the latest lockdown is weaker than in the spring. However, recourse to temporary lay-offs could soon gain ground as just over one in every two firms (excluding the self-employed) said that, in the coming weeks, it would make greater use of temporary lay-offs than currently, in line with the further relaxation of the temporary lay-off scheme.

The proportion of private sector employees working from home has risen considerably between October and November. While in October, 22 % of employees alternated between on-site work and working from home (i.e. partial teleworking), no more than 9 % of them did so in November. With full-time teleworking now the general rule, the share of employees who do all their work from home has risen significantly, up from 21 % in October to 30 % in November. Widening recourse to teleworking is nevertheless not possible for all companies, and the main obstacle mentioned by firms questioned is still the type of work (for 57 % of the respondents). Lack of equipment or inadequate training of employees remain secondary factors (cited respectively by 6 and 2 % of the respondents).

Employees off sick or in quarantine account for 3.4 % of private sector employment, compared with 3.2 % in October and 2.2 % in September. This percentage is clearly higher in sectors where teleworking is not so easy.

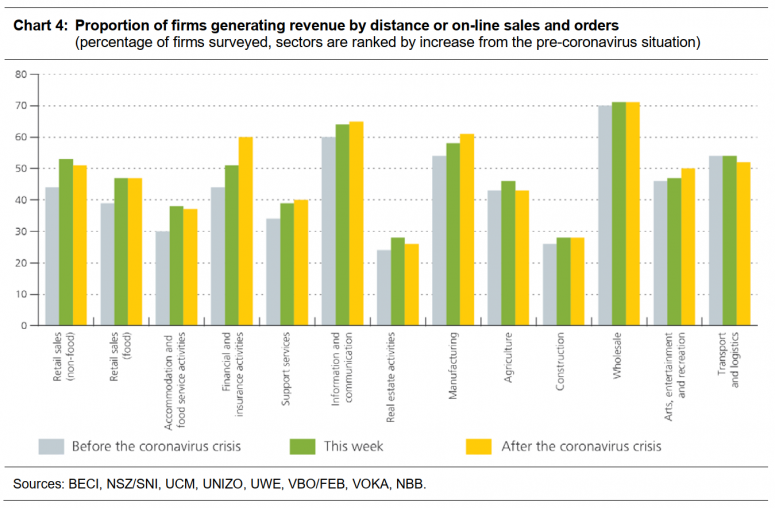

The coronavirus crisis is causing a structural rise in e-commerce

Customers’ fears of getting infected with the virus and the compulsory closure of certain categories of physical sales outlets have led a lot of companies to develop remote sales or on-line ordering systems. The proportion of firms surveyed generating revenue through remote selling or ordering has increased sharply compared with the period before the coronavirus crisis, and especially in consumer-oriented sectors of activity. This percentage has risen by about 8 points in food and non-food retailing, accommodation and food services, financial and insurance activities. It is also up, albeit to a lesser extent (some 4 percentage points) in real estate, support services, information and communication, the manufacturing industry and agriculture. Moreover, this increase is structural, with many firms questioned saying that it would not drop back after the coronavirus crisis and that would even gain further ground in financial and insurance activities. This general trend could also boost the need for a suitable regulatory framework.