Belgian firms see their turnover loss diminish, but many of them face recruitment and supply problems

The loss of turnover due to the coronavirus crisis that Belgian firms report was down from 10 % in May to 8 % in June. The improvement is particularly marked for firms in the hospitality sector, and that is obviously due to the re-opening. The other indicators also show that the impact of coronavirus on the Belgian economy is waning. These are the findings of the last regular ERMG survey of Belgian firms, conducted at the beginning of last week. Nonetheless, there are some serious supply-side problems which could hamper the recovery. For instance, the labour market still exhibits considerable tension, which is particularly acute in the Flemish Region. Furthermore, one firm in two reports moderate to severe disruption of its supplies.

At the beginning of last week, a number of federations representing businesses and the self-employed (BECI, NSZ/SNI, UCM, UNIZO, UWE and VOKA) conducted a new ERMG survey. This initiative is coordinated by the NBB and the FEB/VBO. It was the twenty-second in a series of surveys carried out since March 2020, aiming to assess the impact of the coronavirus crisis and the restrictive measures on economic activity and the financial health of firms. The number of firms taking part was lower than usual (1 936). That slightly increases the margin of error in the results, which should be interpreted with even more caution than usual[1].

Current and projected turnover continued to recover in June

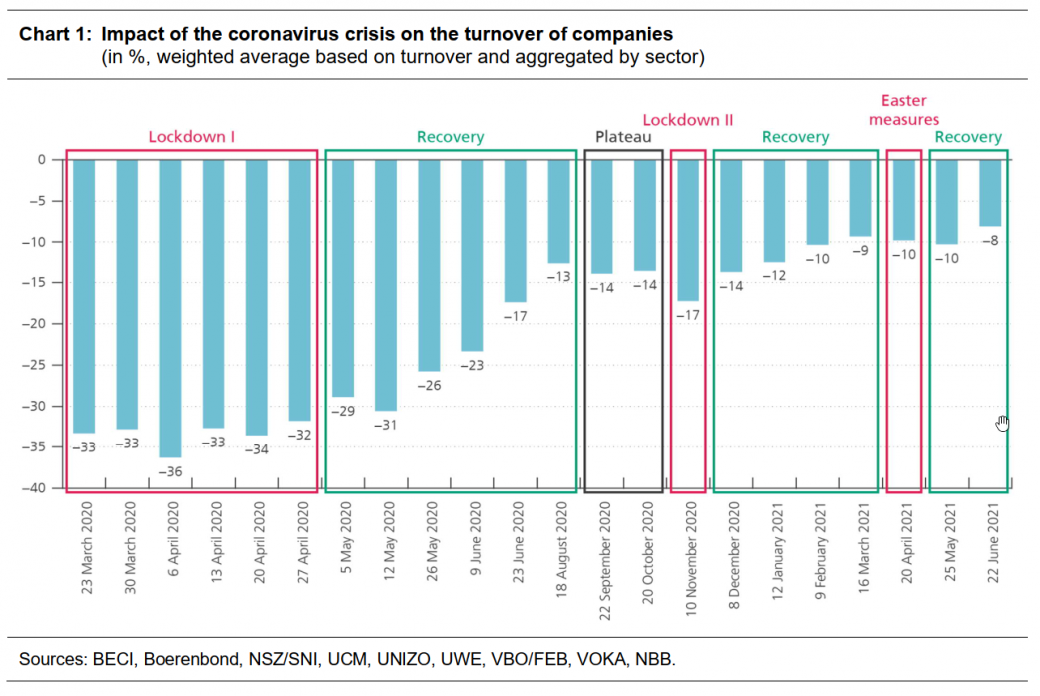

Taking account of firms’ size and sectoral value added, the firms polled last week stated that their current turnover was down by 8 % compared to normal. That is a 2 percentage point improvement compared to the May survey, and is the best result since the start of the crisis.

The June increase in turnover was seen in most industries thanks to the improvement in the health situation and the phasing out of some of the restrictive measures. The rise was by far the most pronounced in accommodation and food service activities where the loss of turnover was more than halved, from almost 70 % in May to 30 % in June. While there was still no significant increase in turnover when only the terraces were reopened in May (perhaps because of the inclement weather), the reopening of indoor areas in June brought a strong revival. Turnover also improved to a lesser extent in the other hard hit branches of activity, particularly travel agencies, road passenger transport, aviation, non-medical contact professions and the arts, entertainment and recreation sector. Most other industries also saw the continuing, gradual restoration of their turnover, almost to the level which would have prevailed without the coronavirus crisis. Only food retailing and non-food retailing reported a decline in their turnover, but that could be due to composition effects within the sample.

[1] The ERMG survey is based on the opinions of the firms taking part. Comparison of the results over time should therefore be interpreted with a degree of caution, because the firms questioned may vary from one survey to the next. First, it is always possible that the federations conducting the surveys of their members may not be the same. Also, firms do not participate systematically in every survey. Although we correct any over-representation in the sample of firms from certain sectors, it is possible that the firms polled may vary according to other characteristics as time goes by. Finally, it should be noted that the survey results take no account of public administration and defence services, education services and human health services.

The turnover forecasts for 2021 improved further, rising by 2 percentage points to 6 % below the level that would have prevailed without the coronavirus crisis. In the knowledge that these figures relate to the year 2021 as a whole and that the turnover loss was still considerably greater in the first half of the year, at an average of 10 %, we can deduce that firms expect strong growth in the second six months. Turnover predictions for 2022 remained stable at around 3.5 % below the level that would have prevailed without the coronavirus crisis, despite a marked improvement for travel agencies and accommodation and food service activities. Nonetheless, these figures still indicate that the coronavirus crisis has caused lasting damage to the economic fabric.

The bankruptcy risk and the employment indicators also displayed a very favourable trend in June

The other indicators also improved, showing that the impact of the coronavirus crisis is waning. For instance, the bankruptcy risk declined considerably for the second consecutive month. The percentage of firms polled which expect to apply for bankruptcy in the next six months was down from 4.8 % in April to 4.0 % in May and 3.2 % in June. Concern over the repercussions of the current situation on commercial activities, measured on a scale ranging from 1 (not very concerned) to 10 (very concerned) also declined further, from 5.6 in May to 5.3 in June.

After having been more or less static for eight months at around 45 %, the proportion of employees working solely at their workplace increased substantially in June to 56 %. That corresponds to the level reached the last summer when the restrictions relating to the first wave of the epidemic had been eased. This increase is attributable partly to a decline in both full-time home working (from 27 % in May to 22 % in June) and part-time home working (from 19 % in May to 16 % in June) and partly to the significant fall in the proportion of workers temporarily laid off (from 5 % to 2 %).

In addition, the labour market indicators also improved in June. In May, the respondents had expected a net increase in private sector jobs of 22 000 units, but in June that increased to 46 000 units. However, these figures concern intended recruitment, but in the absence of suitable applicants they may not be fully reflected in job creation; in that regard, the replies to the questions concerning recruitment difficulties give reason for some caution.

Firms report serious recruitment problems, mainly owing to the lack of applicants

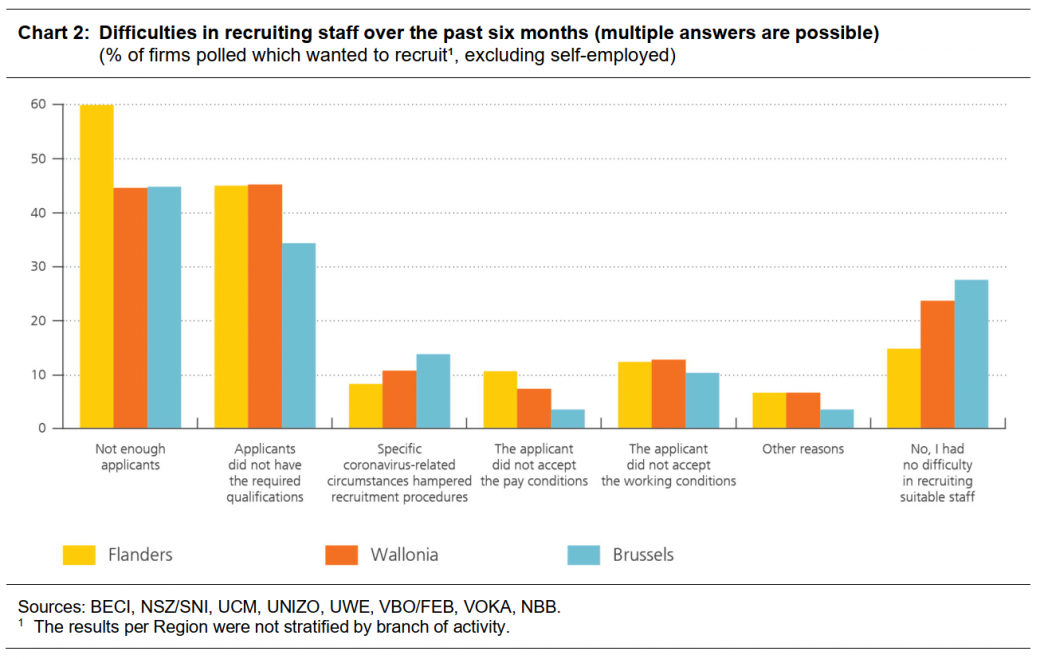

According to the findings of the May survey, firms are having much more difficulty than usual in recruiting staff. That is confirmed by this survey which once again asked about recruitment problems, focusing on firms wishing to recruit within the past six months (60 % of firms). Fewer than one in five of these firms stated that it had no difficulty in recruiting qualified staff over the past six months. That figure is lower for Flanders (15 % of firms) than for Wallonia (24 %) and Brussels (28 %).

The main problems hampering recruitment are the lack of applicants (for 55 % of firms) and the lack of the required qualifications such as technical skills, experience and soft skills (for 45 % of firms). Other factors (such as coronavirus-related circumstances or rejection of pay or working conditions) have had far less impact. However, it should be noted that not only the lack of applicants but also the rejection of pay conditions were reported considerably more often by Flemish firms than by respondents in the other Regions. This may indicate that national wage-setting systems come up against regional variations.

The survey also concerned the strategies used to a greater extent than usual over the past six months to overcome staff shortages. First, firms mainly report that they made more use of external labour, in some cases via consultants, freelance workers, agency staff, students (casual workers) or staff on temporary contracts (28 % of firms), and in other cases by subcontracting to another firm (14 % of firms). In addition, many firms made extra efforts to recruit staff by offering better working conditions, such as flexible working hours, home working and a more congenial workplace (21 % of firms), offering better pay (15 %), recruiting in new geographical areas (8 %) and arranging transport between home and the workplace (2 %). Finally, 20 % of firms state that they have invested more than usual in supplementary training and development for existing staff. Here, too, there are marked regional differences. It was mostly Flemish firms that offered (or had to offer) better pay and recruited in new geographical areas, while it was mainly Brussels firms that offered better working conditions and arranged transport between home and the workplace.

Serious supply problems persist but are not causing a shift in supply chains

The proportion of firms experiencing supply problems has risen sharply since the beginning of this year. Among firms that depend on supplies (two-thirds of the firms polled), half state that their supplies have been moderately or seriously disrupted this month, the same proportion as in the May survey. The branches of activity most affected are wholesale, non-food retail, construction and industry. The most commonly cited reasons for these supply problems are shortages experienced by suppliers (71 % of respondents needing supplies), but transport problems are also mentioned regularly (28 % of respondents needing supplies).

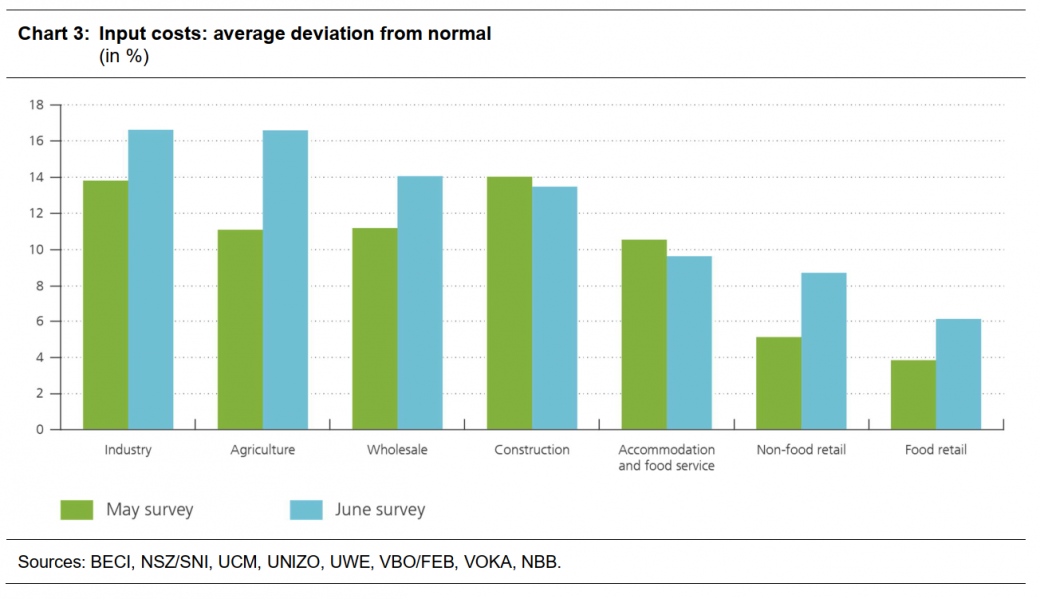

The supply chain problems reported are associated with a steep rise in input costs. For most of the sectors directly affected by such problems, input costs are actually even higher than in May: on average, 17 % higher than normal in industry (compared to 14 % in May), 17 % higher than normal in agriculture (compared to 11 % in May) and 14 % higher than normal in the wholesale trade (compared to 11 % in May).

The June survey also asked about the current location of suppliers before the coronavirus crisis and expectations for the future. There was very little change in the suppliers’ location between the three periods analysed: on average, taking account of firm size, Belgian suppliers account for 61 % of supplies, and suppliers in neighbouring countries (France, Germany, Netherlands and Luxembourg) represent 14 %. The industrial sector, wholesale and non-food retail are naturally more dependent on suppliers in more distant locations, but in their case, too, the evident and expected impact of the coronavirus crisis on the location of suppliers seems to be very small.

The increased use of online sales channels will continue to grow in the coming years

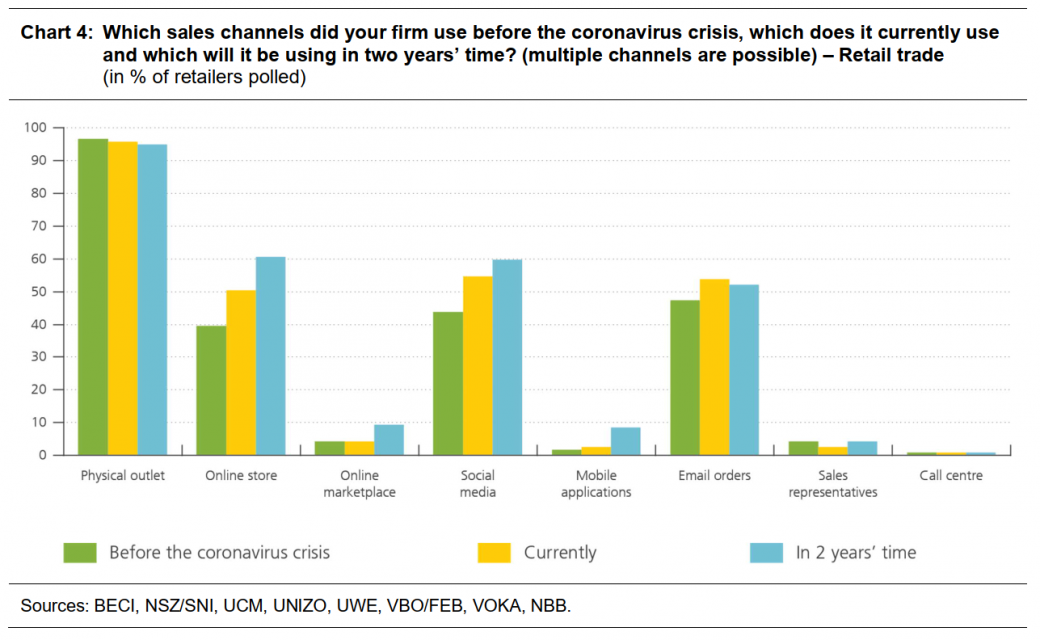

The restrictions imposed by the health crisis obliged many firms to suddenly speed up their digitalisation strategy. In that connection, the June survey measured the change in the use of various sales channels (pre-crisis, currently, and expectations for the next two years).

In the retail sector, the current use of online sales channels is much greater than before the crisis, and this trend will persist in the coming two years. The percentage of firms using mobile applications as a sales channel will be five times as high as in the pre-crisis period, at 9 % of firms within two years; the use of online marketplaces will double to 9 %, and use of the firm’s own online store and social media will increase by half to 60 %. Conversely, the proportion of retailers selling through physical outlets will hardly decline at all over the same period, remaining at around 95 %. The strong growth of online sales channels and the retention of traditional sales outlets also apply to other branches of activity in the Belgian economy.

The end of the ERMG surveys on the coronavirus crisis: thank you to everyone concerned!

This is the last of the regular ERMG surveys. As the economic situation is gradually returning to normal, it was decided to halt this highly labour-intensive survey. An ad hoc retrospective will probably follow in the autumn.

For eighteen months the ERMG survey has been an important instrument for close and rapid monitoring of the impact of the coronavirus crisis on the real economy. The survey data formed a key source of objective information in many discussions on the economic situation.

The NBB would like to thank the partner institutions (FEB, BECI, Boerenbond, NSZ/SNI, UCM, UNISOC, UNIZO, UWE, VOKA) for their close collaboration, and is also particularly grateful to the thousands of self-employed workers and firms who took the time to respond to the survey during this difficult crisis period. The NBB’s Governor Pierre Wunsch states: “We are particularly grateful to all these organisations for their contribution to the surveys. Without their collaboration or feedback, we could never have achieved the high degree of accuracy and representativeness of the ERMG survey findings.”

However, the termination of the ERMG surveys does not mean that we shall not be checking the economy’s pulse in the coming months, during and after the COVID-19 period. The National Bank will continue to do that via its usual analyses and measuring instruments (confidence surveys, Business Cycle Monitor, statistical publications, scientific research, economic projections, annual report, etc.).