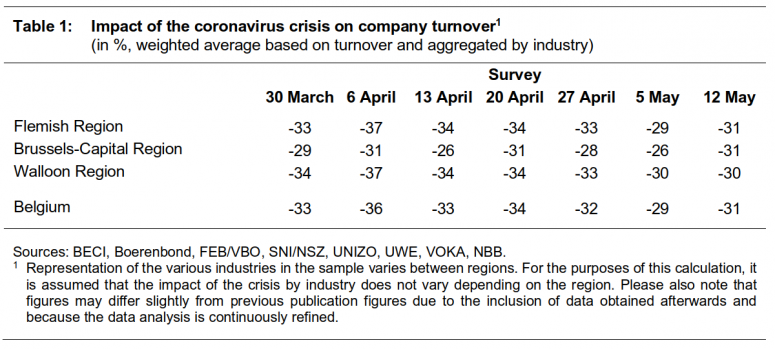

The impact of the crisis on company turnover is still high: recovery of the Belgian economy will take some time

Brussels, May 2020 – With non-food shops reopening on 11 May, turnover in the retail trade sector has bounced back strongly, but it is still well below pre-crisis levels. On the other hand, turnover has continued to fall in other sectors, like information and communication services and some other business-related services. The average drop in turnover for all companies surveyed has not come down any more over the last week and turnover is still around 30 % below pre-crisis levels. That is mainly due to still very weak demand. These are the main findings from the ERMG (Economic Risk Management Group) survey carried out last week after the start of the latest phase of deconfinement began.

For the seventh week in a row, a survey was carried out by a number of federations of enterprises and the self-employed (notably, BECI, UNIZO, UWE and VOKA for this latest survey). This initiative coordinated by the NBB and the FEB/VBO aims to assesses the impact of the coronavirus crisis on economic activity in Belgium and on the financial health and decision-making of Belgian companies week by week. In total, 2 285 enterprises and self-employed people replied to the seventh survey[1].

[1] Participation in the survey by some federations whose members operate in a specific sector of activity may lead to sampling errors. For instance, companies from one by branch of activity could be strongly represented in our sample but not actually have much weight in the economy as a whole. The sample by branch of activity is therefore stratified depending on the weight in value added in Belgium.

Loss of company turnover has not got any smaller, despite the clear improvement observed for non-food retail outlets

After the slight improvement recorded last week, the drop in turnover reported by companies has deteriorated a little. So, it is still around 30 % when account is taken of company size and the weight of the branches of activity in value added in Belgium. Comparing the last two weeks (corresponding to the beginning of the lifting of confinement measures) with the five previous waves of the survey, a slight improvement can be observed, but is still only very marginal given the scale of the shock companies are facing. This suggests that, despite the large-scale restart, the economy is still ticking over very slowly and full recovery will take a long time. The situation in the catering and accommodation and the arts, entertainment and recreation branches is comparable to previous survey findings and is consequently still worrying.

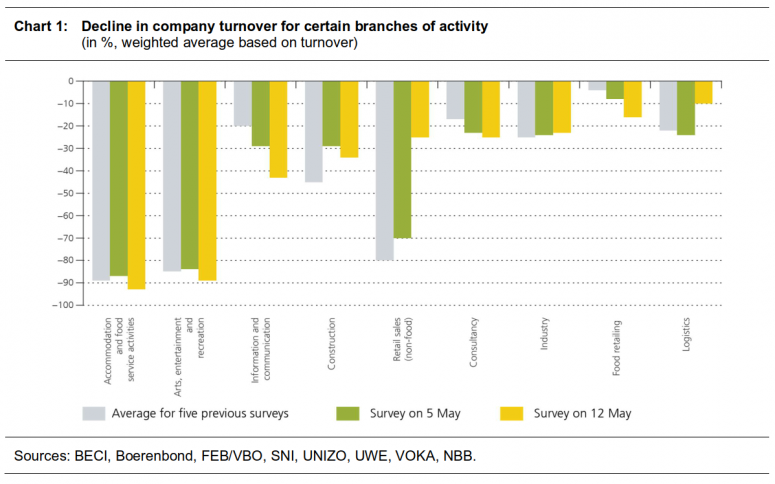

Even though no widespread improvement has been observed in terms of sales turnover, the reopening of non‑food retail outlets on 11 May has had a positive effect on the loss of turnover in the trade sector (-36 % compared with an average of -51 % in the previous weeks) as well as on turnover figures in transport and storage (-19 % compared with an average of -28 % in the previous weeks). The improvement in the latter sector is mainly observed among surveyed firms that are active in logistics and may therefore, at least in some part, be linked to the reopening of non-food shops.

More precisely, the slightly better turnover figures reported by retail firms is driven by those that are active in non-food retail sales, which point to a 25 % drop in turnover this week compared with a fall of almost 70 % on average in the previous weeks. The reopening of a large part of the retail trade sector has thus obviously had a positive effect.

Within other sectors of activity, firms surveyed point to either some stabilisation or a deterioration of their turnover in comparison to the period preceding the lifting of some of the confinement measures. For example, firms questioned in the information and communication services sector report a 43 % drop in turnover from pre-crisis levels, against an average 21 % fall in previous weeks. Whatever the sector considered, there is still a big drop in turnover reported compared with pre-crisis levels.

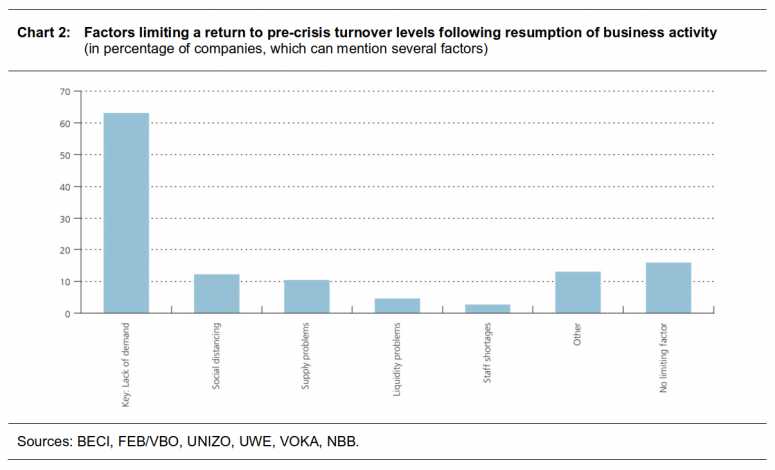

Slack demand is still the biggest obstacle to the recovery

Among the factors that are largely hindering a return to pre-crisis turnover volumes after business activity resumed, it is weak demand that comes up the most often, this element being cited by more than six out of ten firms. This factor is found to be important in the majority of branches of activity and in particular in the transport and storage sector (77 % of respondents) as well as in industry (72 % of respondents). For these sectors, foreign demand is crucial and consequently the slow and only partial recovery of international trade is probably hindering the resumption of their business activity more.

Other factors limiting the rise in turnover are generally less cited by the firms surveyed, but they can be important for certain specific sectors. For instance, difficulty in applying social distancing measures only affects 12 % of respondents but this factor is nevertheless important in the catering and accommodation (59 %), real estate (41 %), arts, entertainment and recreation (38 %) and construction (26 %) sectors. Supply problems, which affect one in every ten firms, are mainly cited in construction (26 %), industry (17 %) and trade (15 %). Finally, cash flow problems and staff shortages seem to have shrunk and are cited by less than 5 % of firms.

The risk of bankruptcy, too has, subsided a little for non-food shops, but has continued to grow for the hardest-hit branches of activity

The perception of risk of bankruptcy is following the same trend as turnover, remaining similar to the average observed over the last few weeks. For example, 8 % of self-employed people or company managers consider that bankruptcy is likely or very likely. Some improvement has been observed in non-retail trade sales: the proportion of firms surveyed mentioning that bankruptcy was likely or very likely for them has dropped from 11 % in the previous survey to 6 % this week. The resumption of activity has therefore led to renewed optimism even though the situation remains alarming.

Firms surveyed in the arts, entertainment and recreation and catering and accommodation sectors point up a high risk of bankruptcy, even higher than in the last few weeks. Within these two sectors, respectively 39 % (compared with 26 % on average in previous weeks) and 24 % (compared with 19 % on average over the last few weeks) of respondents regard the prospect of bankruptcy as likely or very likely.

The degree of concern indicated by companies questioned, measured on a scale of 0 to 10, is down for the second consecutive week, dropping from 7.1 two weeks ago, to 6.9 last week and 6.7 this week.